Centralized Augmented Reality (AR), Virtual Reality (VR), Mixed Reality (MR), Metaverse, Extended Reality (XR) and Spatial Computing Industry Statistics & Analysis - 2026

Executive Summary

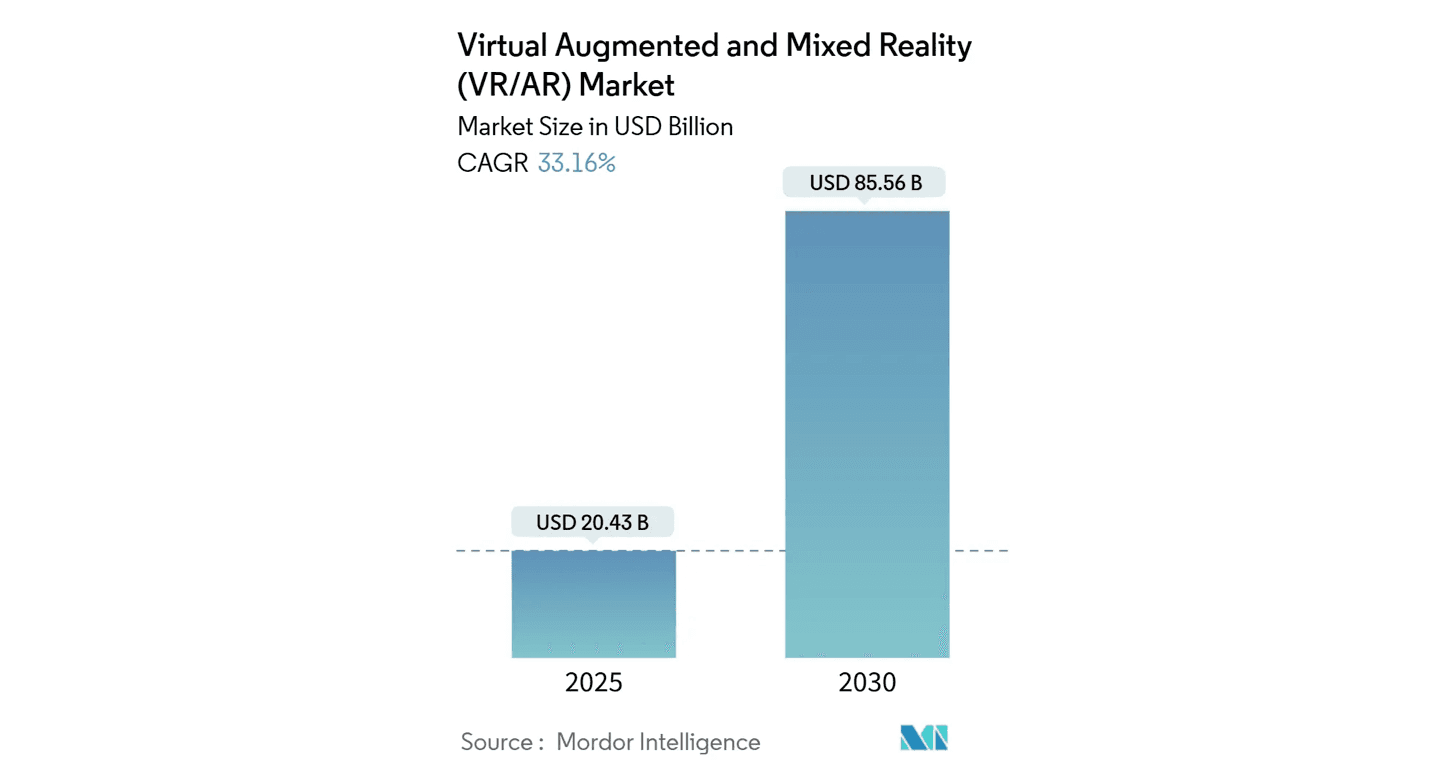

The global spatial computing market is worth $20.43 billion in 2025 and growing toward $85.56 billion by 2030.

TL;DR - Key AR/VR/MR/XR and Spatial Computing Industry Statistics

Metric | Value |

|---|---|

Spatial Computing Market 2025 | $20.43B |

Projected Market 2030 | $85.56B |

XR Device Shipments 2025 | 14.5M (+41.6% YoY) |

Meta Combined XR Market Share | 75.7% |

Enterprise Share of VR Revenue by 2030 | 60% |

Fastest-Growing Region | Asia-Pacific (35.1% CAGR) |

The AR, VR, XR, MR, Metaverse and Spatial Computing industry is moving from pilot projects to production infrastructure. Enterprise adoption is accelerating, XR hardware ecosystems are consolidating around Meta and a handful of challengers, and Asia-Pacific's manufacturing base is pulling ahead of North America on growth rate even as North America leads on absolute market size.

Overview of the Spatial Computing / Extended Reality (XR) Industry

Spatial computing, also called extended reality (XR), lets people interact with computers in three-dimensional space instead of through a screen. The category covers several overlapping technologies, each with distinct characteristics, all pointing toward the same outcome: digital content that sits naturally inside the physical world.

What Counts as AR, VR, MR, XR, Metaverse and Spatial Computing

Spatial Computing refers to the broader technological category that enables digital content to exist and interact within three-dimensional space, using spatial sensors, displays, cameras, artificial intelligence and machine learning to understand and map physical environments. It encompasses XR technologies while also including augmented reality, virtual reality and mixed reality systems.

Extended Reality (XR) serves as an umbrella term synonymous with spatial computing, encompassing all immersive technologies: VR, AR and MR.

Virtual Reality (VR) creates fully immersive digital simulations that completely replace the user's view of the real world, typically through head-mounted displays that block out physical surroundings. Users interact within computer-generated 3D spaces for gaming, training simulations and virtual experiences.

Augmented Reality (AR) overlays digital content onto the real world, enhancing users' perception of their physical environment through smartphones, head mount displays or specialized smart glasses. Augmented reality maintains full awareness of real-world surroundings while adding contextual digital information, objects or interfaces.

Mixed Reality (MR) refers to environments where physical and digital content interact in real time. Often described as a continuum between Augmented Reality (AR) and Virtual Reality (VR), MR blends elements of both. The term covers a wide range of experiences, from fully virtual spaces to light augmented overlays anchored in real environments.

Metaverse, as defined by Meta Platforms, refers to a collective virtual shared space created by the convergence of virtually enhanced physical reality and physically persistent virtual space, including the sum of all virtual worlds, augmented reality and the internet. This definition emphasizes an interconnected, immersive digital environment where people can interact, work and play in real-time, transcending traditional digital boundaries.

Why Industry Statistics Matter

Accurate statistics matter here because spatial computing moves fast enough that stale numbers mislead. Investors evaluating market opportunities, enterprises planning technology adoption and policymakers shaping regulation all rely on current data to make decisions.

Market Size & Growth Projections

Every major spatial computing segment is growing. Multiple research firms forecast compound annual growth rates above 30% across XR categories, driven by enterprise adoption, better hardware and use cases that go well beyond gaming.

Overall Market Valuations

The global spatial computing market is projected to grow from $20.43 billion in 2025 to $85.56 billion by 2030, a 33.16% compound annual growth rate (CAGR), according to Mordor Intelligence. Treeview treats this as the primary market-size figure throughout this report. This combined virtual, augmented and mixed reality market ranks among the fastest-growing technology sectors globally. A separate, more bullish estimate from the same research category projects the market reaching $200.87 billion by 2030 at a 22.0% CAGR from a larger 2024 base. The gap between the two reflects differing assumptions about which product categories count toward the total, and readers should treat the $200.87 billion figure as an upper-bound scenario rather than the consensus case.

Key Statistics: Virtual, Augmented and Mixed Reality Combined Market:

2025: $20.43 billion

2030 primary estimate: $85.56 billion (33.16% CAGR from $20.43B in 2025)

2030 upper-bound estimate: $200.87 billion (22.0% CAGR from $59.76B in 2024)

Segment-Specific Projections

Growth varies by segment. Virtual reality is smaller in absolute terms than the combined market above, but momentum is strong, driven by gaming, training and enterprise applications.

Key Statistics: Virtual Reality Market:

2024: $16.32 billion

2025: $20.83 billion

2032: $123.06 billion

CAGR: 28.9%

AR and VR training is one of the fastest-growing applications in the XR ecosystem, a vertical-specific signal of the enterprise adoption driving the industry as a whole.

Key Statistics: AR and VR in Training Market:

2025: $22.56 billion

2034: $82.92 billion

CAGR: 15.56%

These segment numbers line up with the $85-200 billion 2030 range above: VR makes up a significant share of the combined market, and training keeps outgrowing the ecosystem around it.

Hardware Market & Device Shipments

Hardware is the foundation of the spatial computing ecosystem, and vendor positioning is shifting fast. Meta Platforms still dominates, but new entrants like XREAL are growing quickly in emerging categories like smart glasses.

Market Share Leaders & Growth Trends

Meta held 75.7% of the combined XR device market in 2025, spanning both headsets and smart glasses. Global headset shipments grew 18.1% year-over-year in Q1 2025. Meta's share slipped to 50.8% that quarter, a sign of a more competitive market, while XREAL captured 12.1%, proof that lightweight AR glasses can take real share fast.

Key Statistics - Q1 2025:

Global AR/VR headset market grew 18.1% YoY in Q1 2025

Meta Platforms held 50.8% share that quarter

XREAL captured 12.1% market share in Q1 2025

Across full-year 2024, Meta held a commanding 74.6% share, the payoff of its integrated hardware, software and content ecosystem. Apple's Vision Pro took 5.2% despite its premium price, and Sony Corporation held steady at 4.3% through PlayStation VR2.

Vendor | 2024 Share |

|---|---|

Meta Platforms | 74.6% |

Apple | 5.2% |

Sony Corporation | 4.3% |

ByteDance | 4.1% |

XREAL | 3.3% |

Full-year 2025 figures confirm this, per IDC's Q3 2025 XR Tracker: Meta's 75.7% share holds once smart glasses are counted alongside headsets. Within the standalone VR/MR headset category alone, excluding smart glasses, Meta's share was narrower at approximately 53%, reflecting real competition from Sony, Pico and others in that specific segment. The two percentages measure different things: the 2024 and Q1 2025 figures above cover headsets only, while the 75.7% figure covers the full XR category including smart glasses.

Key Statistics - Full-Year 2025 Vendor Share:

Meta, combined XR including smart glasses: 75.7%

Meta, standalone VR/MR headsets only: 53%

Shipment Volumes & Market Trends

XR device shipments grew 41.6% year-over-year in 2025 to approximately 14.5 million units, reversing the contraction analysts had forecast for the year. 2024 held up well: global AR/VR headset shipments reached 9.6 million units, up 8.8-10% year-over-year depending on methodology. Display panel shipments rose 12%, and Meta Quest grew 11%, validation for its multi-price-point, frequent-update strategy.

Key Statistics - 2024 Performance:

Global AR/VR headset shipments: 9.6 million units

Growth: 8.8%-10% YoY

AR/VR display panels shipments +12% in 2024

Meta Quest shipments up 11% YoY

The anticipated 2025 contraction did not materialize. Smart glasses drove nearly all of the increase, while standalone VR/MR headsets contracted for part of the year before recovering in H2. IDC forecasts continued growth of 33.5% in 2026, with a 26.5% compound annual growth rate for the market between 2026 and 2030.

Key Statistics - 2025-2026 Performance:

2025 XR shipments: 14.5 million units, +41.6% YoY

Smart glasses accounted for roughly half of all 2025 shipments

2026 forecast: +33.5% growth

2026-2030 CAGR: 26.5%

EMEA AR/VR spending is forecast to reach $8.4 billion by 2029 per IDC, driven by growing enterprise adoption and government-backed digital transformation initiatives across the region.

Key Statistics - EMEA Regional Market:

EMEA AR/VR spending forecast to reach $8.4B by 2029

Smart Glasses & AI Glasses

Smart glasses shipped 7.25 million units in 2025, accounting for roughly half of all XR device shipments for the year, up from around 25% of shipments in 2024. The smart glasses category represents the most dynamic segment within the broader XR hardware market, demonstrating explosive growth that signals a paradigm shift toward more socially acceptable form factors. Meta accounts for nearly all of that volume through Ray-Ban Meta and Oakley Meta combined.

Key Statistics - Full-Year 2025 Smart Glasses Performance:

2025 smart glasses shipments: 7.25 million units, roughly 50% of total XR shipments

Ray-Ban Meta and Oakley Meta together account for approximately 97% of AI smart glasses volume

Meta Platforms held >70% share of the total smart glasses market including non-AI models

Meta's Ray-Ban partnership exemplifies the potential for mainstream smart glasses adoption when technology companies collaborate with established fashion brands. Ray-Ban Meta sold an estimated 6.5 million units in 2025 alone, more than the entire AI smart glasses segment shipped in all of 2024, bringing lifetime units to 8.9 million across all generations. The Gen 2 model, launched September 2025 with an upgraded camera and expanded Meta AI integration, drove most of that volume. Oakley Meta HSTN launched the same year and shipped approximately 500,000 units, immediately becoming the second-largest AI smart glasses product on the market.

Platform | Lifetime Units | 2025 Units | YoY |

|---|---|---|---|

Ray-Ban Meta | 8.9M | 6.5M | +225% est. |

Oakley Meta HSTN | 500K | 500K | New |

Ray-Ban Meta accounts for roughly 93% of Meta's own 2025 smart glasses shipments, with Oakley Meta making up the remainder. Smart glasses revenue inside Meta ($2.15B) exceeded Quest hardware revenue ($660M) for the first time in 2025.

In contrast to the smart glasses surge, Apple's Vision Pro momentum continued to decline through 2025. After shipping approximately 390,000 units in its 2024 launch year, Apple sold only 85,000 units in 2025, a 78% year-over-year decline, before halting production at assembly partner Luxshare later in the year. Despite the volume contraction, Vision Pro established that buyers will pay premium prices for high-fidelity spatial computing, and it pushed competitors to improve passthrough display quality. Reports as of early 2026 suggest Apple has shifted its immediate hardware focus toward smart glasses rather than a near-term Vision Pro successor.

Metric | Value |

|---|---|

2024 units | 390,000 |

2025 units | 85,000 (-78% YoY) |

Lifetime units | 475,000 |

Lifetime hardware revenue | $1.66 billion |

Production status | Halted in 2025 |

Content & Developer Economics

Content is the bridge between hardware and actual use. Platform owners are investing billions while developers push for sustainable monetization, and the numbers suggest the industry may finally be closing in on a content economy that can sustain itself.

Meta Quest Ecosystem Performance

Meta Quest is the dominant content ecosystem in VR. Players have spent over $2 billion on Quest titles to date, across more than 4,000 apps in the Meta Store as of 2026, evidence that both the user base and willingness to pay for premium VR content keep growing.

Key Statistics - Developer Revenue & Engagement (2024):

Over $2B has been spent on Meta Quest titles to date

Developer payments increased 12% in 2024

Monthly time in VR increased 30% YoY in 2024

Meta's Oculus Publishing initiative funded and shipped over 100 titles in 2024 alone, with more than 200 currently in production, a bet that hardware adoption ultimately comes down to having good software to run on it.

Key Statistics - Content Production Pipeline:

Meta's Oculus Publishing: 100+ funded titles shipped in 2024

200+ titles currently in production

Apple Vision Pro Ecosystem

Vision Pro has sold approximately 475,000 units cumulatively since its 2024 launch, with enterprise buyers, an estimated 75% of purchases and more than 50 Fortune 100 organizations, outpacing consumer demand. The visionOS ecosystem has grown to more than 3,000 apps, though most are still legacy 2D-style ports rather than true spatial applications. Vision Pro faces the classic chicken-and-egg problem: developers will not build fully spatial experiences until there is a bigger consumer base to build for.

Metric | Value |

|---|---|

Lifetime units | 475,000 (2024: 390,000, 2025: 85,000) |

Lifetime hardware revenue | $1.66 billion |

Enterprise buyer share | 75% |

Fortune 100 orgs using Vision Pro | 50+ |

visionOS apps available | 3,000+ |

Enterprise Adoption & Training

Enterprise adoption is the strongest near-term growth driver in spatial computing. Organizations are seeing measurable ROI from immersive training, guided work, data visualization, digital twins, prototyping and collaboration, the kind of clear payback that consumer markets, still limited by content and social acceptance, have not matched.

Enterprise XR Adoption Statistics

75% of Fortune 500 companies have adopted VR for training and education, a sign the technology has matured enough for hands-on learning, safety training and procedure simulation at scale. Enterprise users are projected to drive 60% of total VR revenue by 2030, a shift away from gaming as the category's main revenue source.

Key Statistics - Fortune 500 Adoption:

Over 75% of Fortune 500 companies have adopted XR through pilot programs or production use

Enterprise will drive 60% of total VR revenue by 2030

Commercial shipments grew 14.9% in 2024

Training Effectiveness & Corporate Implementation

Corporate training is where XR effectiveness data is richest, tracked closely against learning outcomes, time-to-competency and cost. Only 7% of organizations overall actively use VR for training, but that jumps to 22% among large enterprises, scale and resources make successful implementation easier.

Key Statistics - Training Delivery Methods (2024):

VR actively used in training by 7% of organizations overall

VR actively used in training by 22% of large enterprise companies

AR used by 4% of organizations

The evidence for VR training is strong. Learners complete training four times faster than classroom instruction and stay four times more focused than e-learning participants. They report 3.75 times more emotional connection to the material and up to 275% more confidence applying what they learned, and at scale, VR training can cut costs by 52% versus classroom instruction.

Key Statistics - XR for Training Study Results:

Learners completed training 4× faster than classroom

4× more focused than e-learners

3.75× more emotionally connected to content

Up to 275% more confident applying skills

At scale, VR can be 52% less costly than classroom training

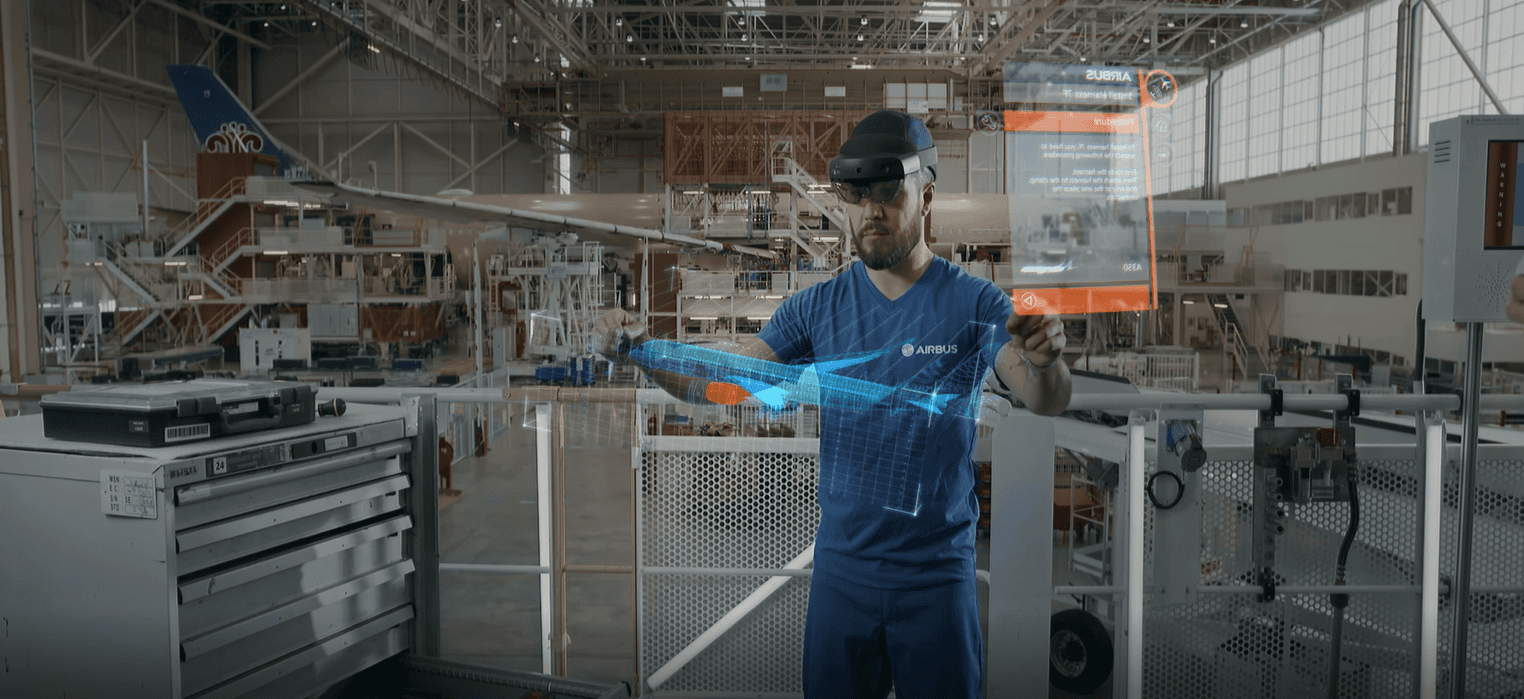

The corporate results back this up. Boeing cut training time per employee by 75% with VR-based assembly training. Airbus saw 25% faster maintenance task performance versus traditional CATIA and DMU methods. Delta Airlines took daily technician proficiency checks from 3 to 150, a 5,000% jump.

Key Statistics - Corporate Success Stories:

Boeing: 75% reduction in training time per person

Airbus: 25% faster maintenance performance vs traditional methods

Delta Airlines: Boosted technician proficiency checks from 3 to 150 per day (5,000% increase)

Healthcare sector: 40% fewer surgical mistakes with VR training

Manufacturing: 43% reduction in workplace injuries

Skilled Trades Training Breakthroughs

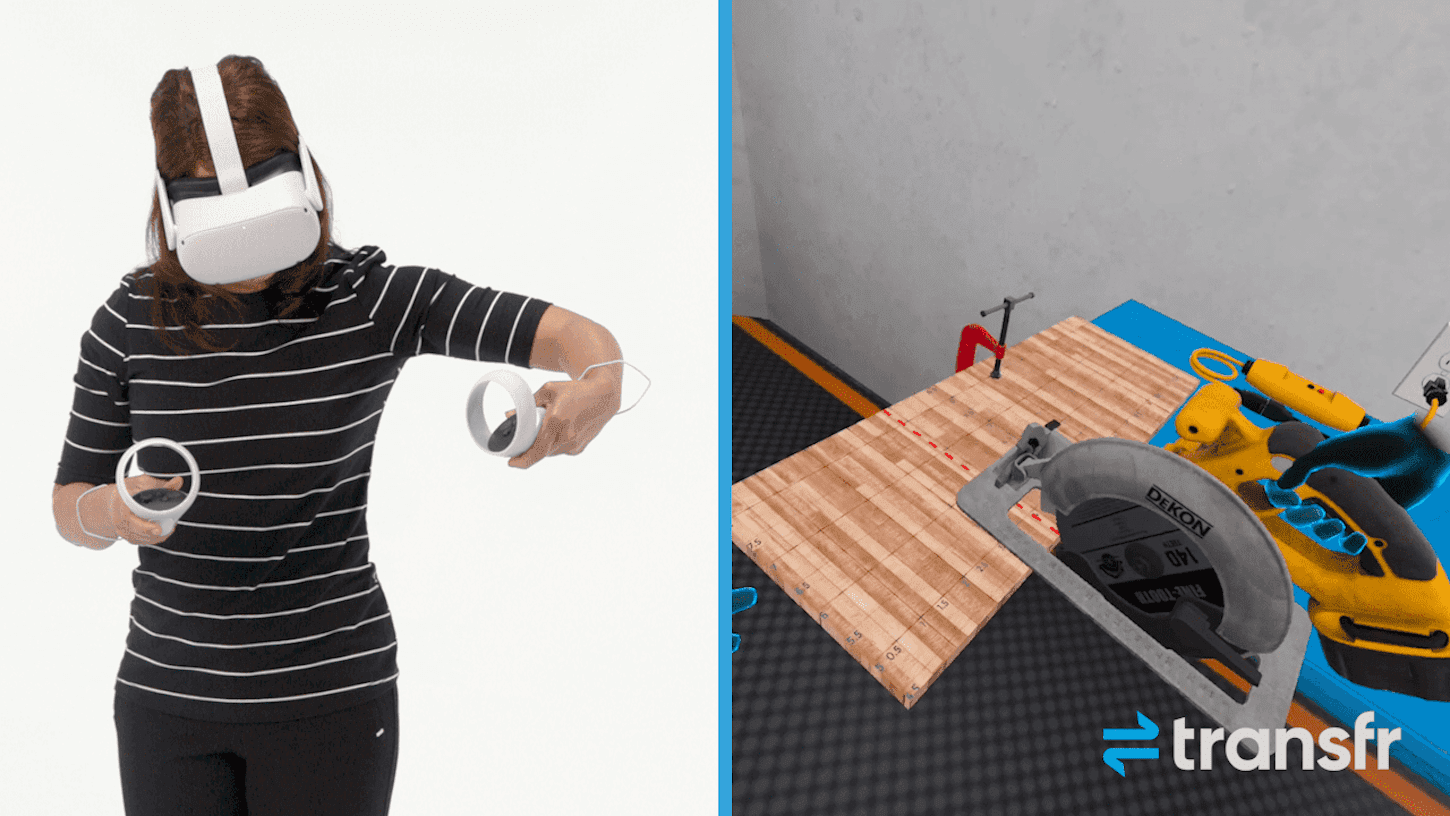

VR training works just as well outside the corporate world, in skilled trades education. Controlled studies show it can compress months of hands-on experience into a fraction of the time, safely, even for hazardous tasks.

VR gets novices to intermediate-level performance fast. In automotive maintenance training, VR-educated beginners performed statistically similar to intermediate technicians trained on video, compressing a learning curve that normally takes months into hours.

Key Statistics - Skilled Trades VR Training Effectiveness:

Oil Change Training: VR-trained novices performed statistically similar to intermediate-level workers with video training

Electrical Construction: VR training showed superior knowledge retention compared to passive video learning

Blood Pressure Training: VR group achieved 78% learning gain vs. 44% for traditional slides (78% improvement)

Respirations Training: VR group achieved 50% learning gain vs. 31% for slides (61% improvement)

Pain Assessment: VR group achieved 47% learning gain vs. 30% for slides (57% improvement)

Temperature Assessment: VR group achieved 37% learning gain vs. 25% for slides (48% improvement)

Construction education backs this up too. NCCER, working with Associated Builders and Contractors of Illinois, compared traditional lab instruction to VR-enhanced learning and found students training on circular saws and electric drills in VR reported significantly higher engagement and a better grasp of safety protocols.

Key Statistics - Construction Training Studies:

NCCER Construction Study: Students reported significantly higher engagement and confidence with VR vs. traditional lab training

Arkansas State Study: 67% of students reported increased confidence, 71% reported positive change in perceived learning

Active vs. Passive Learning: Active VR participation showed statistically superior learning gains vs. passive video watching

Cross-Age Adoption: 90% of users aged 60+ successfully adapted to VR training despite no prior experience

The benefits go beyond knowledge retention. Students consistently say VR gives them a realistic preview of the job before they start it, closing a gap traditional trade education has always struggled with: connecting classroom theory to real-world work.

Key Statistics - Student Engagement and Confidence:

Focus Improvement: Students "put their phones down" and completed modules "without distraction" during VR training

Self-Efficacy: VR training participants reported increased self-efficacy compared to traditional methods

Real-World Connection: Students reported better understanding of "what to expect on the job" through VR simulations

Retention Advantages: VR training showed superior knowledge retention over time compared to traditional instructional methods

Industry-Specific Adoption

Healthcare is one of the most promising vertical markets for AR/VR, spanning medical training, patient treatment and surgical planning. The healthcare AR market has grown from roughly $610 million in 2018 to a projected $4.2 billion by 2026, and 40% of healthcare providers already use VR for patient treatment and staff training.

Key Statistics - Healthcare Industry:

2018 AR market: $610 million

2026 projection: $4.2 billion

40% of healthcare providers using VR for patient treatment/staff training

Education has moved just as fast: 30% of universities worldwide now offer VR-based courses as of 2024, and Meta's push into the segment drove 69.4% growth in educational VR deployments that year.

Key Statistics - Education:

30% of universities worldwide offering VR-based courses in 2024

Education segment grew 69.4% in 2024

Manufacturing shows some of the strongest ROI numbers in XR. The economic value of AR IoT in manufacturing is projected to reach $40-50 billion by 2025 and $90-110 billion by 2030, and 75% of industrial companies running large-scale VR/AR deployments report 10% efficiency gains.

Key Statistics - Manufacturing & Industrial:

Economic value of AR IoT in manufacturing: $40-50 billion by 2025, $90-110 billion by 2030

75% of industrial companies implementing large-scale VR/AR report 10% operations increase

Investment & Funding Landscape

Spatial computing investment tells two different stories. Corporate spending from major tech companies is at unprecedented levels, while venture capital has cooled well off its pandemic-era peak as investors look for sustainable business models and clearer paths to profitability.

Corporate Investment

Meta invested approximately $20 billion in Reality Labs in 2025, about 20% of the company's total budget, making it one of the largest sustained technology investments in recent corporate history. This spending is distributed across hardware development, software platforms, content creation and fundamental research. Reality Labs now allocates roughly 70% of operating expenses to wearables and AI glasses, with the remaining 30% going to VR and Horizon initiatives, a shift from the AR-weighted allocation of prior years.

Metric | Value |

|---|---|

Annual Reality Labs investment | ~$20B (~20% of Meta's total budget) |

Spending split | ~70% wearables/AI glasses, ~30% VR/Horizon |

Cumulative operating losses since 2020 | $83.6B |

Cumulative revenue since 2020 | $11.8B |

Full-year 2025 revenue | $2.27B |

Q4 2025 revenue / operating loss | $955M / $6.02B loss |

Venture Capital Activity

VC investment in XR peaked in 2021-2022, riding broader tech-sector enthusiasm and metaverse hype. 2021 was the sector's second-best year ever at $3.9 billion, behind only 2018's record $4.4 billion, and Q4 2021 alone set a single-quarter record of $1.9 billion.

Key Statistics - Historical Investment Peaks:

2021: $3.9 billion (second-best year ever)

2018: $4.4 billion (best year on record)

Q4 2021: $1.9 billion (record quarter)

Since then, investment has retreated hard. Metaverse-related funding fell to roughly $760 million by Q3 2022, a steep correction driven by slower-than-expected consumer adoption, hardware limitations and open questions about sustainable business models in consumer VR.

Key Statistics - Recent Trends:

Q3 2022: $760 million

Investment cooling due to slower consumer market adoption rates

Focus shifting to AI-enabled applications

Notable Recent Deals

Strategic partnerships and enterprise deals are still pulling in real money despite the broader cooldown. Google put $150 million into a Warby Parker partnership for AI-powered smart glasses, $75 million of it earmarked for co-development. Meta committed $100 million to Anduril for U.S. defense XR deployments, and ArborXR raised a $12 million Series A while acquiring competitor InformXR.

Key Statistics - 2025 Major Partnerships:

Google LLC + Warby Parker: $150M AI-powered smart glasses ($75M co-development)

Meta Platforms + Anduril: $100M U.S. defense XR deployments

ArborXR Series A: $12M + InformXR acquisition

Regional Market Analysis

Adoption, government support and competitive positioning vary sharply by region. North America still leads on absolute market size and venture capital activity, but Asia-Pacific is growing faster, powered by manufacturing capacity, government initiatives and fast-expanding consumer markets.

Geographic Distribution

North America still leads on absolute revenue and market share, holding 27.8-35.53% of global market value depending on methodology. The U.S. alone is projected to generate $12.57 billion in AR/VR revenue in 2025, backed by a strong venture capital ecosystem, significant defense spending and the concentration of major tech companies driving both innovation and adoption.

Key Statistics - North America (2024):

Market share: 27.8%-35.53%

U.S. leads with $12.57 billion projected 2025 revenue

Strong VC ecosystem and defense spending

Asia-Pacific is the fastest-growing region, projected at a 35.1% CAGR through 2030. The region's XR market is expected to expand from $28.46 billion in 2024 to $238.37 billion by 2032, a 30.43% CAGR, driven by China's manufacturing and distribution scale, Japan's technology base and government support for digital transformation across the region.

Key Statistics - Asia-Pacific:

Fastest growing region: 35.1% CAGR through 2030

2024: $28.46 billion, 2032 projection: $238.37 billion (30.43% CAGR)

Led by China's manufacturing and Japan's tech innovation

Government support through policy initiatives

China plays both sides: it is a major consumer market and the dominant supplier of XR hardware components. The government has designated XR a "future industry" and backs it with provincial R&D grants, manufacturing scale, domestic demand and policy support all pointing the same direction.

Key Statistics - China Specific:

Major distributor of HMDs and VR hardware

Government designates XR among future industries

Provincial R&D grants supporting ecosystem development

Japan combines advanced technology infrastructure, a strong gaming culture and growing healthcare adoption, and is expected to post the fastest growth rate in the Asia-Pacific VR market over the forecast period, helped by 5G infrastructure that enables AR/VR platforms.

Key Statistics - Japan:

Expected fastest growth in APAC VR market

Advanced gaming culture and healthcare adoption

5G infrastructure supporting AR/VR platforms

Market Penetration Rates

Europe is showing particularly strong momentum. The European AR/VR market is projected to grow from $2.8 billion in 2021 to $20.9 billion in 2025, VR/AR is expected to enhance more than 400,000 jobs in Germany and the UK by 2030, and the European AR software market is forecast to hit $3.8 billion by 2027.

Key Statistics - European Market Growth:

European AR/VR market: $2.8B (2021) → $20.9B (2025)

400,000 jobs to be enhanced in Germany/UK by 2030

European AR software market: $3.8B projected by 2027

AR gaming segment in Europe: $1.8B projected by 2027

U.S. consumer adoption shows what a mature market looks like: 48% of consumers have tried VR, 13% of households own a headset, and among owners, 88% use their device multiple times a month and 60% use it more than once a week. Adoption skews young: 35% of 25-34 year-olds have used VR.

Key Statistics - U.S. Consumer Adoption:

48% of U.S. consumers have VR experience

13% of U.S. households own VR headset

88% of VR owners use device multiple times monthly

60% use it more than once weekly

30% bought VR device "to see what the hype was about"

35% of 25-34 year-olds have used VR technology

The numbers below track user engagement and market penetration as spatial computing reshapes both industries and everyday consumer experience.

Key Statistics - Global User Statistics:

AR/VR user penetration expected to reach 56.5% by 2029

Expected users: 3.728 billion by 2029

Average revenue per user (ARPU): $13.3

Industry Applications & Use Cases

Spatial computing applications span every major industry vertical, but adoption looks different depending on whether the use case is consumer entertainment or enterprise productivity, some sectors have real user adoption, others are still in pilot phase.

Primary Application Areas

Gaming still dominates VR use: 70% of headset owners play games on their devices. But usage has diversified well beyond entertainment: 42% watch films or TV, 35% use VR for workouts or exercise, and 22% use it for creative work like music, video or art.

Key Statistics - Usage Distribution:

Gaming: 70% of VR headset users

Films/TV watching: 42% of VR device owners

Workouts/exercise: 35% of VR headset owners

Creative activities: 22% use for music, video, art creation

Healthcare: 41% of VR devices

Education: 41% of VR devices

Entertainment and gaming remain the largest revenue category, at 38.3% of total market revenue in 2024. The XR gaming market alone hit $18 billion by 2023, helped by VR arcades and location-based entertainment venues that let people try high-end experiences without buying a headset.

Key Statistics - Entertainment & Gaming:

Entertainment & Gaming are the leading category with 38.3% of 2024 revenue

XR gaming market: $18 billion by 2023

VR arcades and location-based entertainment growing

Healthcare is the fastest-growing vertical application, projected at a 33.9% CAGR on the back of proven clinical outcomes. The healthcare XR market is expected to triple by 2030, backed by case studies showing a 50% reduction in patient pain scores and $200,000 in monthly savings from reduced medication use.

Key Statistics - Healthcare Growth:

Healthcare is the fastest growing enterprise vertical: 33.9% CAGR

Healthcare XR market size to triple by 2030

50% reduction in pain scores

$200,000 monthly savings in pain medication costs

Emerging Applications

Real estate is a clear practical fit: the VR/AR real estate market is projected to reach $80 billion by 2025, roughly 1.4 million registered agents already use VR for client presentations, and 40.4% of apartment buyers say panoramic tours influence their decision, with 72.7% rating the VR tour experience positively.

Key Statistics - Real Estate:

Estimated $80 billion VR/AR real estate market value by 2025

1.4 million registered agents using VR technology

40.4% of apartment buyers influenced by panoramic tours

72.7% positive feedback on VR tours

Retail and e-commerce show measurable business impact from AR: roughly 100 million shoppers used AR in 2020, AR try-on experiences reduce return rates, and virtual showrooms drive higher basket sizes than traditional e-commerce, all without requiring anything beyond a smartphone.

Key Statistics - Retail & E-commerce:

100 million shoppers used AR in 2020

Reduced return rates with AR try-on experiences

Virtual showrooms achieving basket-size uplifts

Job Market & Economic Impact

The spatial computing (XR) industry demonstrates strong employment growth and competitive compensation. VR developers in the United States earn an average salary of $108,471 per year, while job postings for AR/VR roles have increased 154% over the past five years. Meta's Reality Labs division generated $2.27 billion in revenue in 2025, while the company has sold more than 20 million Meta Quest headsets cumulatively.

Employment Projections

The United States is positioned to lead global job creation in spatial computing, with projections indicating 2.32 million AR/VR jobs by 2030. This represents extraordinary growth from a 2019 baseline of just 800,000 jobs globally, suggesting a potential 2,775% expansion over the decade. International projections are even more ambitious, with industry analysts forecasting 23 million XR-related jobs worldwide by 2030, spanning roles from content creators and experience designers to specialized technicians and enterprise implementation consultants.

Key Statistics - Job Creation:

2.32 million AR/VR jobs projected in U.S. by 2030

Global projection: 23 million jobs by 2030

2019 baseline: 800,000 jobs (2,775% growth potential)

Average VR developer salary in U.S.: $108,471 per year

154% increase in AR/VR job postings over past 5 years

Economic Value Creation

Virtual reality's contribution to global economic value demonstrates the technology's transformation from an emerging technology to significant economic driver. VR added $13.5 billion to the global economy in 2022, with projections indicating growth to $138.3 billion by 2025. The most ambitious forecasts suggest combined AR and VR technologies could contribute $1.59 trillion to global economic output by 2030, with AR alone accounting for $1.09 trillion and VR contributing $450.5 billion.

Key Statistics - Economic Value:

2022: VR added $13.5 billion to global economy

2025: Projected $138.3 billion contribution

2030: Combined AR/VR projected $1.59 trillion boost

AR alone: $1.09 trillion, VR: $450.5 billion

Meta Reality Labs: $2.27B total revenue in 2025

Meta has sold >20 million Meta Quest headsets cumulatively

Industry Impact by Sector

Beyond gaming applications, XR technologies demonstrate significant productivity improvements across key economic sectors. Workforce development leads growth applications with 24% annual expansion, followed by manufacturing at 21%, automotive at 19% and marketing/advertising at 16%. Engineering applications show particularly strong efficiency gains, with 10% reductions in time-to-market and 7% decreases in construction time, demonstrating concrete business value that justifies enterprise investment.

Key Statistics - Key Growth Sectors (Beyond Gaming):

Workforce development: 24% growth rate

Manufacturing: 21% growth rate

Automotive: 19% growth rate

Marketing/Advertising: 16% growth rate

Engineering: 10% time-to-market reduction, 7% construction time decrease

Industry Competitive Landscape

The spatial computing (XR) industry competitive landscape reflects a complex ecosystem where established technology giants compete alongside specialized studios and product startups, with success increasingly depending on vertical market expertise and integrated platform strategies rather than hardware specifications alone. For a full analysis of the leading companies in the industry see: Best Augmented Reality Companies 2025 and Best Virtual Reality Companies 2025.

Leading Hardware Companies

Meta

Meta maintains the dominant market position through its vertically integrated ecosystem approach, combining proprietary silicon development with the Horizon OS platform and integrated app store. The company's strategy of heavy R&D investment despite sustained operating losses demonstrates long-term commitment to platform dominance, though recent market share fluctuations suggest increasing competitive pressure from new entry competitors.

Apple

Apple has established its premium market positioning with the Vision Pro. The company's silicon-to-services integration strategy draws on its existing ecosystem and distribution advantages, though mass market penetration remains limited by premium and early adoption positioning. Industry reports suggest Apple is developing a more accessible mainstream model targeted for 2027 release.

Google has re-entered the industry through the $250 million acquisition of HTC's XR assets and development of the Android XR platform in partnership with industry hardware leader MagicLeap. The company's approach emphasizes smart glasses applications and partnerships with established eyewear brands, positioning for longer-term market development as hardware form factors evolve toward mainstream acceptance.

Company | Strategy | Key Metric | Market Position |

|---|---|---|---|

Meta | Vertically integrated: proprietary silicon, Horizon OS, app store | 75.7% combined XR market share (2025) | Dominant across headsets and smart glasses |

Apple | Premium silicon-to-services integration | 475,000 lifetime Vision Pro units, production halted 2025 | Premium niche, mainstream model targeted for 2027 |

Platform and partnership model via Android XR | $250M HTC XR asset acquisition | Positioning for the smart glasses era through eyewear partnerships |

Leading Software Companies

XR specialized software companies have become increasingly critical in defining the value of spatial computing by enabling enterprise adoption, integration, and deployment at scale. These firms provide the software development services that turn AR/VR hardware into valuable business solutions and consumer applications.

For more details on the leading AR/VRXR/Spatial Computing software development companies see: Top Spatial Computing Development Companies, Top Augmented Reality (AR) Development Companies and Top Virtual Reality (VR) Development Companies.

Treeview

Treeview is an established leader in AR/VR/XR/MR and spatial computing software development for enterprise companies, focusing on research-driven innovation and industry-specific applications. Treeview's approach emphasizes delivering high-quality custom applications with business value through healthcare, digital twins, training, education and energy use cases, positioning it as a trusted partner for large-scale digital transformation. Treeview’s senior-only development model and reputation for world-class quality reinforce its role as a high-impact software player in the global XR ecosystem.

Accenture

Accenture has built a strong presence in spatial computing by integrating XR solutions into its broader digital transformation and workforce enablement services. Drawing on its consulting expertise and global reach, the firm helps enterprises deploy immersive training, design, and collaboration at scale. Despite challenges in balancing innovation with operational efficiency, Accenture continues to be recognized integrator for XR adoption across Fortune 500 companies.

Capgemini

Capgemini has developed a growing XR practice that aligns with its consulting-driven approach to digital transformation. By focusing on industry-specific integrations, the company supports clients in areas like manufacturing, retail, and energy, where immersive technologies deliver measurable ROI. Capgemini's strength lies in its ability to bridge advanced XR software with enterprise-scale deployment, though it faces increasing competition from both global consultancies and specialized XR studios.

Company | Focus | Differentiator |

|---|---|---|

Treeview | Enterprise XR/AR/VR/MR and spatial computing development | Senior-only development model; healthcare, digital twins and training specialization |

Accenture | Enterprise digital transformation and workforce enablement | Consulting-led, Fortune 500-scale deployments |

Capgemini | Industry-specific XR integrations | Manufacturing, retail and energy verticals, consulting-driven |

Emerging Leaders & Specialists

The competitive landscape increasingly rewards domain-specific expertise over generalist platform strategies. Treeview has emerged as a global leader in enterprise XR and spatial computing R&D, helping large organizations pilot and deploy advanced immersive solutions. ManageXR delivers enterprise-grade device management and analytics to support large-scale XR deployments. Transfr specializes in immersive training and education, providing scalable XR simulations that enhance workforce readiness and career development. Felix & Paul have built a reputation as pioneers in cinematic VR storytelling and immersive entertainment experiences.

Domain-Specific Leaders:

Treeview: Enterprise XR/AR/VR/MR/Spatial Computing app development, R&D and innovation

ManageXR: Enterprise device management + analytics

Transfr: Training and Education

Felix & Paul: Entertainment and storytelling

Sources and Methodology

Hardware shipment, revenue and market share figures were refreshed in July 2026 against full-year 2025 data from IDC's Q3 2025 XR Tracker, Meta's Q4 and full-year 2025 earnings call, and EssilorLuxottica's investor disclosures, the same primary sources used in Treeview's XR & Smart Glasses Market Statistics Report. Where the two reports cover the same hardware data, the numbers are kept identical rather than independently re-derived.

Broader market sizing comes from Mordor Intelligence and Grand View Research. Enterprise adoption, training effectiveness and skilled trades figures are drawn from PwC, Accenture, NCCER and the peer-reviewed studies listed below. Investment and funding figures come from Crunchbase and company funding announcements. Regional figures combine IDC's regional breakdowns with market-research publications specific to each region. These broader figures are current as of January 2026 unless a specific number notes otherwise.

Where two credible sources disagree, such as the two 2030 market-size projections earlier in this report, both figures are stated and the one this report treats as primary is identified rather than picked silently. Where full-year 2025 data has superseded an earlier-year or partial-year figure, hardware shipment volumes and Meta Reality Labs financials being the clearest examples, the current figure is used and the prior figure is not carried forward.

Mordor Intelligence - Virtual, Augmented and Mixed Reality Market Report

Market Research Future - AR and VR in Training Market Report

S&P Global Market Intelligence - AR/VR Installed Base Outlook

Counterpoint Research - Global XR/AR/VR Headsets Market Share, Quarterly

PwC - Virtual and Augmented Reality Could Deliver a $1.4 Trillion Boost, 2020

Meta for Developers - GDC 2025: Opportunities in MR/VR on Meta Horizon OS

BestInXR - Best XR Venture Capital Investors, VCs and Funding in AR/VR and Spatial Computing

GlobeNewswire - Aviation AR/VR Market to Reach $23.6B by 2031, Allied Market Research

Transfr - VR Oil Change Training Shows Better Learning Gain Than Video

BusinessWire - Transfr's VR Simulations Boost Learning Gains in Healthcare Training

International Journal of Educational Technology in Higher Education - Article s41239-022-00349-3

ResearchGate - The Effectiveness of Virtual Reality Training: A Systematic Review

Springer - Virtual Reality Journal Article s10055-023-00843-7

EdTech Innovation Hub - Transfr's VR Training Enhances Healthcare Learning Outcomes

GoingVC - Exploring the AR/VR Revolution: Opportunities, Challenges and Venture Capital Perspectives

DataBridge Market Research - Asia-Pacific Virtual Reality Market

MarketDataForecast - Asia-Pacific Virtual Reality Gaming Market

Frequently Asked Questions (FAQs)

Q1. What are the key trends in the spatial computing, AR/VR, XR, Metaverse market for 2026?

The XR market in 2026 is defined by the mainstream rise of smart glasses, deeper integration of artificial intelligence and rapid improvements in display technology. Consumer-friendly devices like Meta's Ray-Ban smart glasses signal growing demand for stylish wearables, while AI makes XR experiences more intuitive through real-time object recognition, gesture control and generative content. Advances in micro-LED displays and waveguide optics are enabling lighter, more immersive headsets. Together with expanding use cases in healthcare, training and gaming, these trends mark XR's shift from niche innovation to a central technology shaping both enterprise and consumer markets.

Q2. Which companies hold a significant share in the spatial computing, XR, AR/VR, Metaverse industry?

The largest players in spatial computing split into hardware, software and specialized solution providers:

Meta, Apple and Google - hardware innovation through headsets and smart glasses

Treeview, Accenture and Capgemini - enterprise applications, platforms and solutions

Treeview, ManageXR, Transfr and Felix & Paul Studios - domain-specific use cases including enterprise XR research, device management, immersive training and cinematic VR storytelling

Q3. What types of consulting and deployment services are available in spatial computing, XR, AR/VR and Metaverse?

Consulting and development services in spatial computing typically cover the full lifecycle of immersive solutions: discovery and consulting, spatial product design, 3D content creation, custom software development and ongoing support. Deployment services focus on system installation, device and software integration, training and managed services, ensuring reliable operation once a solution is live.

Q4. How does spatial computing, XR and AR/VR provide a competitive edge to businesses?

Spatial computing offers a competitive edge by enabling immersive, interactive experiences that improve productivity, training efficiency and customer engagement. Advanced sensors and digital worlds let businesses streamline operations, reduce costs and innovate across industries including healthcare, manufacturing and retail.

Q5. What are the concerns regarding sensitive data in XR?

Data privacy and security are a real concern given how much spatial and biometric data XR devices collect. Companies are investing in encryption, secure cloud infrastructure and privacy-enhancing technologies to protect user data and stay compliant with regulatory requirements.

Q6. What is the significance of the AR VR MR XR spatial computing statistics industry report 2026?

This report gives stakeholders a single, current reference for market size, growth trends, technology adoption and competitive landscape across AR, VR, MR and XR, useful for anyone making decisions that depend on where the industry actually stands right now.

Q7. How do AR devices contribute to the growth of the spatial computing market?

AR devices, smart glasses and headsets alike, expand spatial computing by overlaying digital content onto the physical world. They drive enterprise adoption, improve training outcomes and enable new use cases across healthcare, manufacturing and retail.

Q8. What role does modeling software play in spatial computing solutions?

Modeling software makes accurate, interactive 3D content possible in AR, VR and MR applications, powering realistic simulations, digital twins and immersive experiences that bridge digital and physical environments.

Q9. How is edge computing impacting the spatial computing industry?

Edge computing processes data closer to the user or device, cutting latency and enabling real-time interaction. It supports complex spatial mapping, AI-driven analytics and cloud integration, the infrastructure behind smoother, more responsive immersive experiences.

Q10. How does the spatial computing industry address concerns around sensitive data?

Through encryption, secure cloud infrastructure and privacy-enhancing technologies, paired with compliance to regulatory standards and transparent data management, especially in sensitive sectors like healthcare and defense.

Q11. What is the regional outlook for the spatial computing market, particularly in North America and the Middle East and Asia?

North America leads on enterprise adoption, technological innovation and software ecosystem maturity. The Middle East and Asia region is emerging fast, backed by government initiatives and growing demand for immersive technologies. Both regions are driving expansion through continued investment in hardware, software and managed services.

Q12. Which companies are major players in the spatial computing industry?

Leading companies include:

Microsoft Corporation

Meta Platforms

Apple Inc.

Google LLC

Treeview

ManageXR

Transfr

Sony Corporation

Lenovo Group Limited

Magic Leap

Unity Technologies

Q13. How do consulting and deployment services support spatial computing market growth?

Consulting provides strategic guidance, technology integration and customized solutions. Deployment covers system installation, integration of spatial computing devices and software, training and managed services, together they turn a strategy into something actually running in production.

Q14. What are digital twins and how are they related to spatial computing?

Digital twins are virtual replicas of physical assets or environments, built using spatial computing technologies to enable real-time monitoring, simulation and analysis. They are one of the clearest examples of spatial computing's core idea: connecting the digital and physical worlds directly.