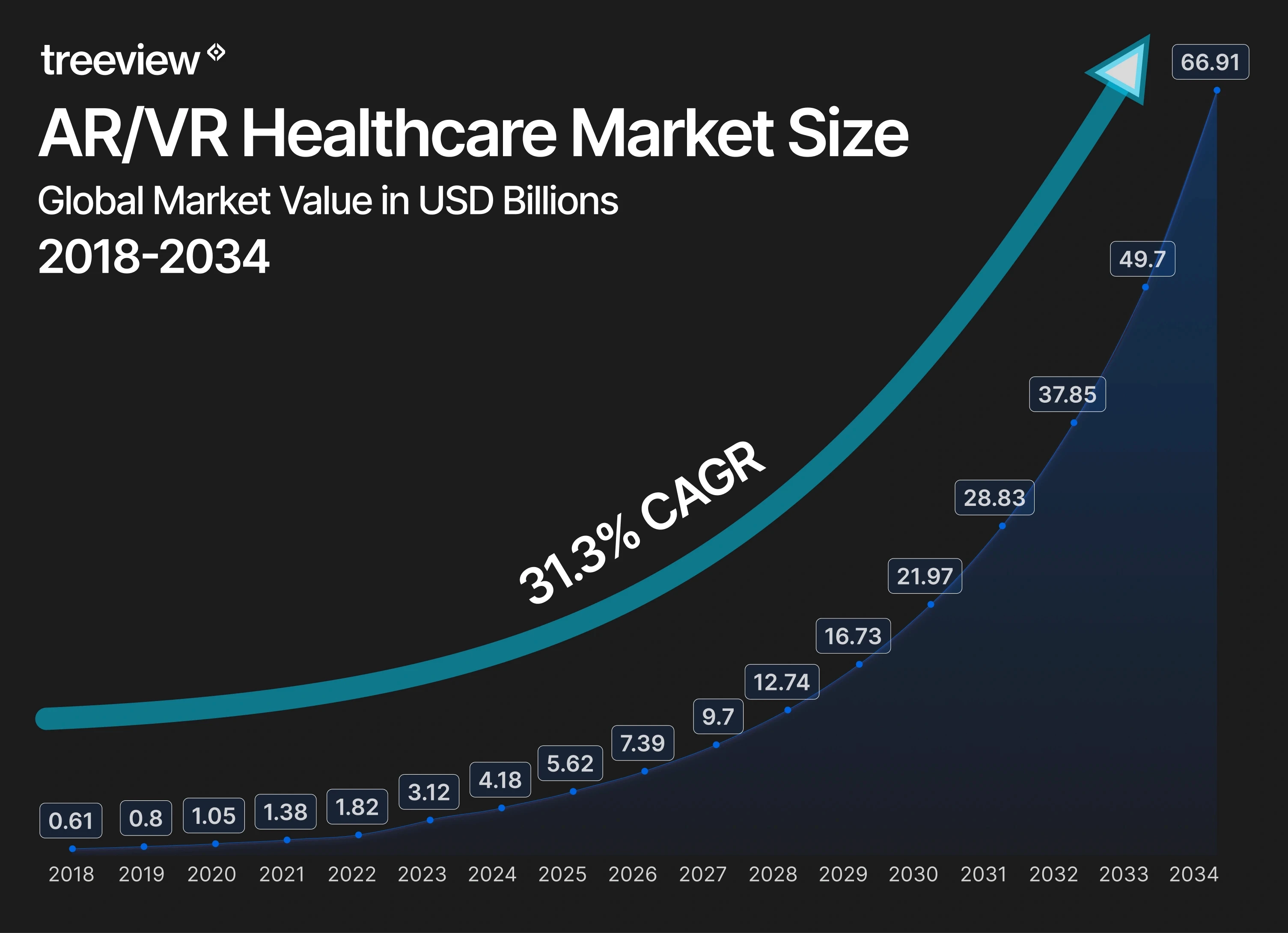

The global VR in healthcare market reached $5.62 billion in 2025, is growing at a 31.3% CAGR and is projected to reach $66.91 billion by 2034 (Fortune Business Insights). The FDA has cleared 110 AR and VR medical devices since 2015. VR-trained surgeons record 40% fewer procedural errors. The AR in healthcare segment is growing at a 33.9% CAGR, the fastest of any XR vertical.

A burn patient undergoing wound care reports 35-50% less pain when a VR headset is involved. That finding has been replicated across dozens of clinical studies, documented in peer-reviewed literature and cited by the CDC as a case for non-pharmacologic pain intervention. It is one data point inside a healthcare technology market that went from $610 million in 2018 to $5.62 billion in 2025.

This report compiles the key statistics on virtual reality in healthcare for 2026: market size by segment and region, FDA-cleared AR and VR medical devices, clinical outcomes across surgical training, pain management, mental health and rehabilitation, hardware deployment data and Treeview's direct observations from building enterprise healthcare XR applications.

TL;DR: Key AR & VR in Healthcare Statistics

Metric | Value |

|---|---|

VR in Healthcare Market (2025) | $5.62B |

VR in Healthcare Market (2026 projection) | $7.58B |

Projected VR in Healthcare (2034) | $66.91B |

VR in Healthcare CAGR | 31.3% |

AR in Healthcare CAGR (fastest vertical) | 33.9% |

VR Medical Simulation Market (2022) | $2.7B |

Projected VR Medical Simulation Market (2031) | $29.6B |

Surgical Simulation Market 2025 | $3.85B |

Projected Surgical Simulation Market 2035 | $15.31B |

VR Pain Reduction in Burn Wound Care | 35-50% |

Monthly Cost Savings via VR Pain Management | $200K+ |

Healthcare Providers Using VR for Training | 40% |

US Hospitals Using AR/VR for Training & Surgical Support | 70% |

Healthcare Organizations Planning or Using VR for Training | 77% |

FDA-Cleared AR/VR Medical Devices (2015-2026) | 110 |

Meta Quest Global Market Share (standalone VR) | 53% |

Virtual reality in healthcare is tracked in this report across market size, segment growth, hardware deployment, clinical outcomes and enterprise adoption. Use cases covered include medical training, surgical simulation, augmented reality in surgery, pain management, mental health and rehabilitation.

AR & VR in Healthcare: Market Overview

The VR in healthcare market reached $5.62 billion in 2025 and is projected to reach $7.58 billion by end of 2026, growing to $66.91 billion by 2034 at a 31.3% CAGR (Fortune Business Insights).

The augmented reality in healthcare only segment tracks AR hardware, software and services in clinical contexts, growing from approximately $610 million in 2018 to a projected $4.2 billion by 2026 at a 33.9% CAGR, the fastest vertical growth rate in the broader XR industry (Mordor Intelligence). For broader XR industry context, see the XR and spatial computing industry statistics report.

Throughout this report, "AR in healthcare" references the narrower segment; "AR/VR in healthcare" references the combined market.

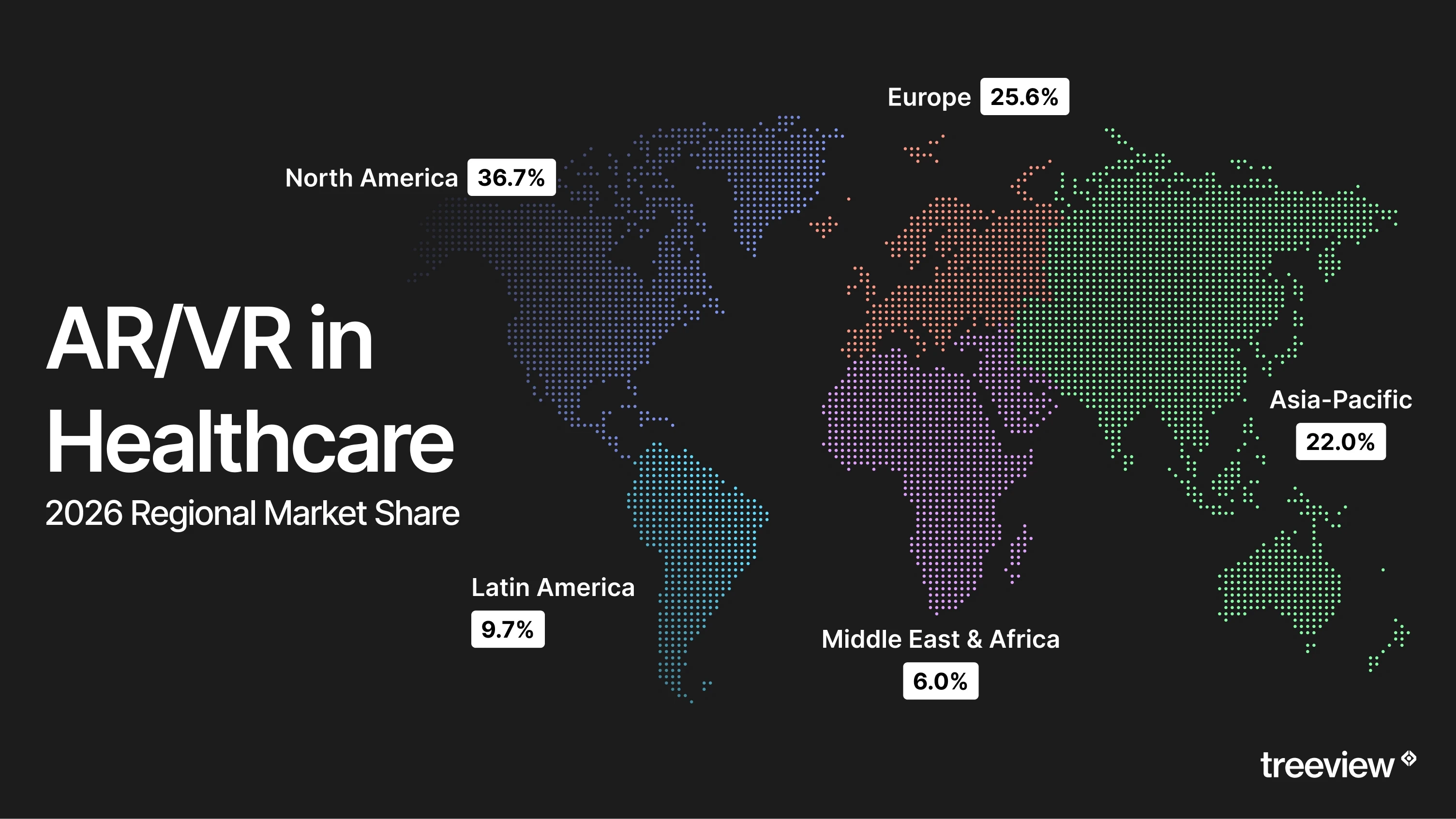

Regional Breakdown

The AR/VR in healthcare market is distributed across five regions, with North America and Europe together accounting for over 62% of global demand in 2025:

North America leads with $2.06 billion (36.7% share), driven by government R&D funding and deep clinical adoption.

Europe holds $1.44 billion (25.6%), led by UK, France and Germany.

Asia Pacific accounts for $1.24 billion (22.0%) and is projected to record the highest CAGR of any region during the forecast period, with China ($0.864B by 2026), Japan ($0.385B) and India ($0.285B) as the primary growth engines.

Latin America ($0.55B, 9.7%) and Middle East & Africa ($0.34B, 6.0%) represent the remainder, with both regions showing accelerating investment in digital health infrastructure.

Region | Share (2025) | Market Size 2025 | 2026 Projection | Key Driver |

|---|---|---|---|---|

North America | 36.7% | $2.06B | $2.75B | Rising VR adoption in clinical practice; US government R&D funding |

Europe | 25.6% | $1.44B | $1.93B | Second-largest healthcare investment region; UK, France, Germany lead VR/AR R&D |

Asia Pacific | 22.0% | $1.24B | $1.71B | Highest CAGR; China, India, Japan driving growth through digital health investment |

Latin America | 9.7% | $0.55B | $0.73B | Growing R&D investment; digital transformation in Brazil, Argentina, Mexico |

Middle East & Africa | 6.0% | $0.34B | $0.46B | UAE, Saudi Arabia, Qatar investing in AI, IoT and VR for healthcare |

AR/VR in Healthcare: Market Segments

The VR in healthcare market breaks into two primary components (hardware and software), three device categories (HMDs, GTDs, PWDs), five application segments, and three end-use institution types. Patient care management holds the largest revenue share by application; surgical training holds the highest CAGR.

Component Breakdown: Hardware vs. Software

The AR/VR in healthcare market splits into hardware and software. Hardware includes head-mounted displays, gesture-tracking devices, and positional wearables. Software includes clinical applications, simulation platforms, therapeutic programs, and content libraries.

Hardware dominated in 2024, accounting for over 47% of total VR in healthcare revenue (Grand View Research). The software segment is growing faster as hospital install bases mature and institutions move from single-department pilots to enterprise-wide deployments requiring platform subscriptions, content updates and integration services.

Component | 2024 Revenue Share | Growth Driver |

|---|---|---|

Hardware (HMDs, GTDs, PWDs) | 47% | Institutional fleet build-out, new headset releases |

Software (platforms, therapeutics, content) | 53% (remainder) | Enterprise scaling, SaaS models, AI-integrated platforms |

Device Segment Breakdown

Three device categories define the AR/VR in healthcare hardware market, each serving distinct clinical functions.

Head-mounted displays (HMDs) are the dominant device segment and the primary deployment vehicle for VR in clinical training, surgical simulation, and patient therapy. Standalone HMDs like the Meta Quest series have displaced tethered systems as the enterprise standard due to lower setup friction, lower cost per unit, and no requirement for a connected PC in clinical environments.

Gesture-tracking devices (GTDs) include hand-tracking gloves and optical hand-tracking systems. GTDs are most relevant in surgical simulation, where haptic feedback and precise instrument handling are clinical requirements. Meta Quest headsets increasingly integrate optical hand-tracking natively, reducing the need for separate GTD hardware.

Positional and wearable devices (PWDs) include full-body tracking systems and wearable sensors. PWDs are used in rehabilitation and physical therapy, where tracking patient movement through a range of motion is the clinical objective.

Device | Primary Use Case | Market Position |

|---|---|---|

Head-mounted displays (HMDs) | Surgical training, therapy, patient education | Dominant segment |

Gesture-tracking devices (GTDs) | Surgical simulation, haptic training | Growing, increasingly integrated into HMDs |

Positional/wearable devices (PWDs) | Rehabilitation, physical therapy, motion tracking | Specialist segment |

Application Segment Breakdown

The most frequently misread data point in the healthcare AR/VR market: surgical training has the highest CAGR, but patient care management has the largest current revenue share as of 2024 (Grand View Research). These are compatible: surgical training is growing fastest from a smaller base, while patient care management generates the most revenue because it spans the broadest clinical workflows.

Application | Revenue Position | Notes |

|---|---|---|

Patient care management | Largest segment by revenue (2024) | Spans VR therapy, pain management, patient education, mental health |

Surgical training & simulation | Highest CAGR | ACGME mandates and device company adoption driving rapid growth |

Rehabilitation & therapy | Strong and growing | Stroke recovery, orthopedic rehab, neurological disorders |

Medical education | Established | University programs, residency curricula, CME |

Surgical planning & navigation | Specialist segment | AR-integrated, high per-unit value |

The patient care management dominance matters for enterprise buyers. The clinical ROI case for patient-facing VR (pain reduction, medication cost savings, patient satisfaction scores) is often easier to quantify for hospital CFOs than training ROI, which requires longer-term tracking of complication rates and credentialing cycle time.

US Market: Separate CAGR

The US AR/VR in healthcare market is growing at a 26% CAGR through 2030, somewhat below the global rate of 30.3%, reflecting the market's relative maturity compared to fast-growing Asia-Pacific regions (Grand View Research). North America accounted for over 36% of global VR in healthcare revenue in 2024.

The US-specific slowdown is not a sign of weakness. The US market started earlier and is now in a scale phase rather than an initial adoption phase. Enterprise procurement cycles, HIPAA compliance requirements, and EHR integration complexity slow deployment velocity compared to markets earlier in the adoption curve.

End-Use Deployment: Where AR/VR Is Actually Operating

AR/VR in healthcare is deployed across three primary institution types.

Hospitals and clinics represent the largest end-use segment by revenue. Enterprise procurement is driven by surgical training programs, patient care applications, and rehabilitation units. The shift from individual department pilots to system-wide procurement is the most significant structural change underway in this segment as of 2025-2026.

Research and academic institutions are the primary early adopters and clinical validation engines. Medical schools, university hospitals, and dedicated simulation centers generate the peer-reviewed outcomes data that subsequently drives hospital procurement. ACGME simulation mandates have made this segment structurally significant rather than purely experimental.

Other settings include military medical training (a significant early adopter of VR simulation since the early 2010s), corporate and pharma field force training (Medtronic, Stryker, Daiichi Sankyo), home-based therapy programs (EaseVRx / RelieVRx), and outpatient clinical programs.

End-Use | Market Position | Key Driver |

|---|---|---|

Hospitals and clinics | Largest segment | Enterprise procurement, patient care applications |

Research and academic institutions | Strong, structurally growing | ACGME mandates, clinical validation pipeline |

Military medical | Established, specialist | Long-standing simulation investment |

Pharma and medical device companies | Significant but undercounted in market reports | HCP training, field force education |

Home-based / outpatient | Emerging | FDA-cleared therapeutics, telehealth integration |

Research Firm Comparison: Making Sense of the Market Size Numbers

Market size figures for VR in healthcare vary across research firms because they measure different scopes. This table allows direct comparison rather than treating each figure as contradictory.

Research Firm | Base Year & Value | Projection | CAGR | Scope Notes |

|---|---|---|---|---|

Fortune Business Insights | $5.62B (2025) | $66.91B by 2034 | 31.3% | VR in healthcare: hardware + software + services |

Grand View Research | $5.62B (2024) | $29.38B by 2030 | 30.3% | VR in healthcare: shorter forecast window |

Verified Market Research | -- | $87.42B by 2032 | 39.36% | VR in healthcare: broadest scope definition |

MarketDataForecast | ~$5B (2025, combined) | $47.58B by 2033 | 32.33% | AR + VR in healthcare combined |

DataM Intelligence | $5.03B (2025) | $16.34B by 2033 | 15.8% | Excludes surgical robotics and AI diagnostics |

Mordor Intelligence | $4.2B (2026 est.) | Growing at 33.9% | 33.9% | AR in healthcare only (narrower scope) |

Fortune Business Insights and Grand View Research use the same 2024 base ($5.62B) but different forecast endpoints. Verified Market Research is the most bullish and reflects the broadest scope. DataM Intelligence is the most conservative, explicitly excluding adjacent markets. Mordor Intelligence is the narrowest, covering augmented reality only.

For consistency across Treeview's healthcare content, the Fortune Business Insights figures serve as the primary reference: $5.62B in 2025, growing to $66.91B by 2034 at a 31.3% CAGR.

Hardware & Headsets in Healthcare

VR and AR in healthcare are delivered through two device categories: purpose-built medical AR systems cleared for specific clinical applications (surgical navigation, therapeutic VR), and mass-market enterprise headsets adapted for healthcare workflows. Mass-market enterprise headsets drive the majority of training, simulation, and patient care deployments by unit volume.

Global Headset Market Context

Meta Quest holds 53% of the global standalone VR headset market, with 26.76 million units sold across all models through 2025 (IDC Q3 2025, via Treeview XR Market Statistics Report). Meta Quest is the most widely deployed headset in clinical training environments, simulation labs, and patient therapy programs by volume. Hardware composed over 47% of total VR in healthcare market revenue in 2024 (Grand View Research) and 49.4% of the global VR in healthcare market (Fortune Business Insights).

Meta Quest

Meta Quest is the dominant standalone VR headset in clinical training and healthcare simulation. Meta Quest's enterprise positioning is driven by four factors: standalone operation requiring no connected PC, the lowest per-device cost of any clinically viable headset, native hand-tracking, and the Quest for Business MDM framework allowing hospital IT teams to provision and manage device fleets from a centralized dashboard.

Meta Quest supports clinical simulation across nursing programs, surgical residencies, EMT training and pediatric care education. Purdue Global's School of Nursing deployed Meta Quest to support over 4,000 graduate nurses, with a documented 10-15% increase in the national nursing exam pass rate. Meta Quest is trusted by institutions including Children's Hospital Los Angeles (CHLA) and leading clinical simulation platforms.

Key specifications (Meta Quest 3): Standalone. Snapdragon XR2 Gen 2. 4K+ Infinite Display. Native color passthrough MR. Hand tracking. SOC 2-compliant MDM via Quest for Business (Microsoft Intune, Ivanti, VMware Workspace ONE). Starting at $499 (consumer) / enterprise pricing through Quest for Business.

Primary healthcare use cases: Nursing simulation, surgical residency training, emergency medicine scenarios, patient education, pharma field force training, anatomy visualization.

Apple Vision Pro

Apple Vision Pro is the highest-fidelity mass-market headset entering healthcare workflows, positioned at $3,499. Senior leaders at Elsevier, Philips, Cedars-Sinai Health System, and Boston Children's Hospital have all documented early programs using visionOS in clinical environments, per Fast Company reporting.

Apple Vision Pro's clinical use cases include medical imaging and pathology review (infinite canvas for DICOM data), surgical planning and procedure rehearsal in immersive 3D, clinical education and anatomical visualization, and patient-facing mental health and wellness experiences. The FDA cleared Apple's Digital Prism Correction Feature for Apple Vision Pro twice (October 2024 and June 2025), establishing Apple Vision Pro's first formal regulatory presence as a medical accommodation tool.

Key specifications: Dual micro-OLED displays (23M pixels total). M2 + R1 chips. EyeSight passthrough. Eye, hand, and voice input. 2-hour battery (external). $3,499.

Primary healthcare use cases: Medical imaging review, surgical planning, clinical education, patient experience, executive and academic institution pilots.

Microsoft HoloLens 2

Microsoft HoloLens 2 is the most clinically validated AR headset by published research volume. A systematic review of HoloLens 2 in medical and healthcare contexts (Palumbo, MDPI Sensors, 2022) found that 60% of published HoloLens 2 clinical studies focused on surgical navigation, with medical training and tele-mentoring accounting for a further 19%. Microsoft HoloLens 2 is the reference platform for intraoperative AR overlay applications.

Key Microsoft HoloLens 2 clinical deployments include Project Convergence (Microsoft, Verizon, Medivis, and the VA health system), which delivered the first 5G mixed reality surgical navigation system for veteran healthcare; SentiAR's CommandEP cardiac electrophysiology guidance system (FDA-cleared July 2023); and multiple surgical navigation systems that received FDA 510(k) clearance with HoloLens 2 as the display hardware.

Microsoft has publicly signaled it is not developing a HoloLens 3. Institutional interest has shifted toward Apple Vision Pro and Varjo for optical see-through AR applications.

Key specifications: Holographic optical waveguide display. Inside-out tracking. Spatial mapping. Hand and eye tracking. 2-3 hour battery. $3,500.

Primary healthcare use cases: Intraoperative AR surgical navigation, tele-mentoring, anatomy visualization, medical device training, veteran healthcare (VA system).

Varjo XR-4

Varjo XR-4 is the highest-fidelity commercial MR headset available as of 2025-2026, and the headset of choice for healthcare simulation programs where visual accuracy is a clinical requirement. Varjo XR-4 is sold exclusively to enterprise organizations at $9,990 (Focal Edition) and requires a Varjo account linked to an organization to operate.

Varjo XR-4 delivers 51 PPD (pixels per degree) display resolution, exceeding the human foveal acuity threshold. Varjo XR-4's LiDAR-based depth sensing and 200Hz eye tracking produce mixed reality environments with near-photorealistic fidelity, sufficient for anatomical detail, instrument interaction and spatial positioning in high-stakes procedural rehearsal.

The refreshed Varjo XR-4 Series (October 2025) introduced a redesigned headband and improved comfort for extended training sessions. The Varjo XR-4 Secure Edition is TAA-compliant and supports offline mode for regulated healthcare environments.

Key specifications: 3840 x 3744 per eye (51 PPD). LiDAR depth sensor. 200Hz eye tracking. Full-dome optics. PC-tethered. $5,490 (XR-4) / $9,990 (Focal Edition).

Primary healthcare use cases: High-fidelity surgical simulation, medical device procedural training, collaborative OR team training, defense medical, research environments.

Pico 4 Ultra Enterprise

Pico 4 Ultra Enterprise is the second-largest standalone VR headset platform globally, holding 5% of global VR/MR market share and 46% of China's consumer VR market in H1 2025 (IDC). Pico 4 Ultra Enterprise is designed for business deployment with the PICO Business suite, app sideloading, MDM support, and 4K resolution at a 105-degree field of view. Pico is primarily deployed in healthcare markets where Meta Quest is less accessible, particularly China and parts of Asia-Pacific. Pico received FDA clearance as the headset platform for AppliedVR's RelieVRx (August 2025 clearance covering the Pico G3).

Key specifications: 4K resolution per eye. 105-degree FOV. Wireless. Snapdragon XR2 Gen 2. PICO Business suite. ~$599 (enterprise).

Primary healthcare use cases: Therapeutic VR (RelieVRx), clinical training in Asia-Pacific markets, enterprise simulation.

Headset Comparison: Healthcare Deployment

Headset | Type | Price | Primary Healthcare Role | HIPAA/MDM | Notable Clinical Deployments |

|---|---|---|---|---|---|

Meta Quest 3 | Standalone VR/MR | $499+ | Training, simulation, patient care | Quest for Business (SOC 2) | Purdue Global (4,000+ nurses), CHLA, SimX, UbiSim |

Apple Vision Pro | Standalone spatial | $3,499 | Medical imaging, surgical planning, education | HIPAA: in progress | Cedars-Sinai, Boston Children's, Philips, Elsevier |

Microsoft HoloLens 2 | Tethered AR | $3,500 | Intraoperative AR navigation, tele-mentoring | HIPAA-configurable | VA system (Project Convergence), SentiAR, Medivis |

Varjo XR-4 | PC-tethered MR | $5,490-$9,990 | High-fidelity surgical simulation | TAA-compliant (Secure Edition) | Medical simulation centers, defense medical |

Pico 4 Ultra Enterprise | Standalone VR | ~$599 | Therapeutic VR, Asia-Pacific training | PICO Business MDM | RelieVRx (FDA-cleared), Asia-Pacific clinical programs |

Smart Glasses in Healthcare

Smart glasses in healthcare provide hands-free AR functionality for clinicians who need to remain fully present in their physical environment. Unlike VR headsets, which immerse the user in a separate environment, smart glasses overlay information onto the clinician's real-world field of view. The three primary use cases are intraoperative recording and tele-mentoring, point-of-care documentation and remote expert guidance in distributed or resource-constrained settings.

The global healthcare AR and VR glasses market was valued at $594 million in 2025 and is projected to reach $1.697 billion by 2034 at a CAGR of 16.6% (Intel Market Research). A narrower estimate from 360iResearch places the market at $271 million in 2025, growing to $434 million by 2032 at a 6.95% CAGR.

Clinical Validation

The most significant 2025 smart glasses development is the peer-reviewed validation of consumer-grade smart glasses in an active surgical setting. A study published in Surgical Innovation documented the use of Ray-Ban Meta smart glasses during limb preservation and reconstructive foot and ankle surgery at Adventist Health White Memorial Hospital and the Keck School of Medicine at USC over 18 months (November 2023 to April 2025).

Key findings from the Ray-Ban Meta surgical study:

Ray-Ban Meta smart glasses proved intuitive and unobtrusive within the surgical environment.

First-person footage captured by Ray-Ban Meta smart glasses was judged more instructive by residents than conventional overhead or laparoscopic video.

Voice command activation ("capture photo," "start video") allowed documentation without breaking surgical flow.

This is the first peer-reviewed study to formally validate consumer-grade smart glasses in a sterile surgical workflow.

Enterprise Smart Glasses: Vuzix, RealWear, and Purpose-Built Devices

Vuzix M400 is the most widely referenced smart glasses platform in clinical telemedicine literature. A systematic review in npj Digital Medicine (2025) identified Vuzix as the primary platform cited across telemedicine and remote surgical guidance studies. Vuzix M400 is designed for all-day clinical wear, with a high-definition camera, voice commands, and telemedicine application integrations.

RealWear Navigator 500 is deployed in hospital settings requiring hands-free operation in PPE-compatible configurations. RealWear Navigator 500 is used by paramedics and emergency physicians connecting with senior clinicians in real time while maintaining full situational awareness.

Documented smart glasses clinical use cases:

Remote surgical mentoring: A specialist views a live first-person Vuzix M400 feed and provides real-time audio guidance to an on-site surgeon without requiring the surgeon to look away from the field.

Telemedicine in underserved settings: A PubMed study on smart glasses in spinal surgery in East Africa documented feasibility for remote training in low- and middle-income countries.

Emergency department triage: A clinical trial at Sir Run Run Shaw Hospital (China) found AR smart glasses facilitated faster patient admission workflows vs. standard two-way radio.

Intraoperative AR guidance: AR overlays projected via smart glasses provide real-time anatomical markers, reducing navigation errors in orthopedic and neurosurgical procedures.

The Consumer-to-Clinical Pipeline

The Ray-Ban Meta surgical study signals that the line between consumer and clinical smart glasses is blurring. Ray-Ban Meta smart glasses are an off-the-shelf consumer product, not a medically certified device. Hospitals piloting AR glasses for endometriosis surgery (BBC, 2026) are doing so with devices not FDA-cleared for surgical use. LBMC's 2025 analysis noted that Ray-Ban Meta smart glasses are not designed with HIPAA-level safeguards, creating tension between clinical utility and data governance requirements.

The trajectory points toward a purpose-built clinical tier of smart glasses: devices combining the form factor of Ray-Ban Meta with end-to-end encryption, HIPAA-compliant storage and FDA clearance pathways. No such device had reached commercial scale as of mid-2026.

Key Smart Glasses Devices in Clinical Use

Device | Manufacturer | Primary Use Case | Clinical Deployment |

|---|---|---|---|

Vuzix M400 / M4000 | Vuzix | Telemedicine, surgical guidance, training | Active clinical deployments globally |

RealWear Navigator 500 | RealWear | Emergency medicine, PPE-compatible environments | Hospitals and paramedic services |

Ray-Ban Meta Gen 2 | Meta / EssilorLuxottica | Intraoperative recording, tele-mentoring | Peer-reviewed validation 2025 (USC, Adventist Health) |

Rokid Glass 2 | Rokid | Emergency department triage (China) | Clinical trial (Sir Run Run Shaw Hospital) |

Strolll AR Glasses | Strolll | Neurological disorder assistance (Parkinson's, MS) | Clinical development stage (funded 2025) |

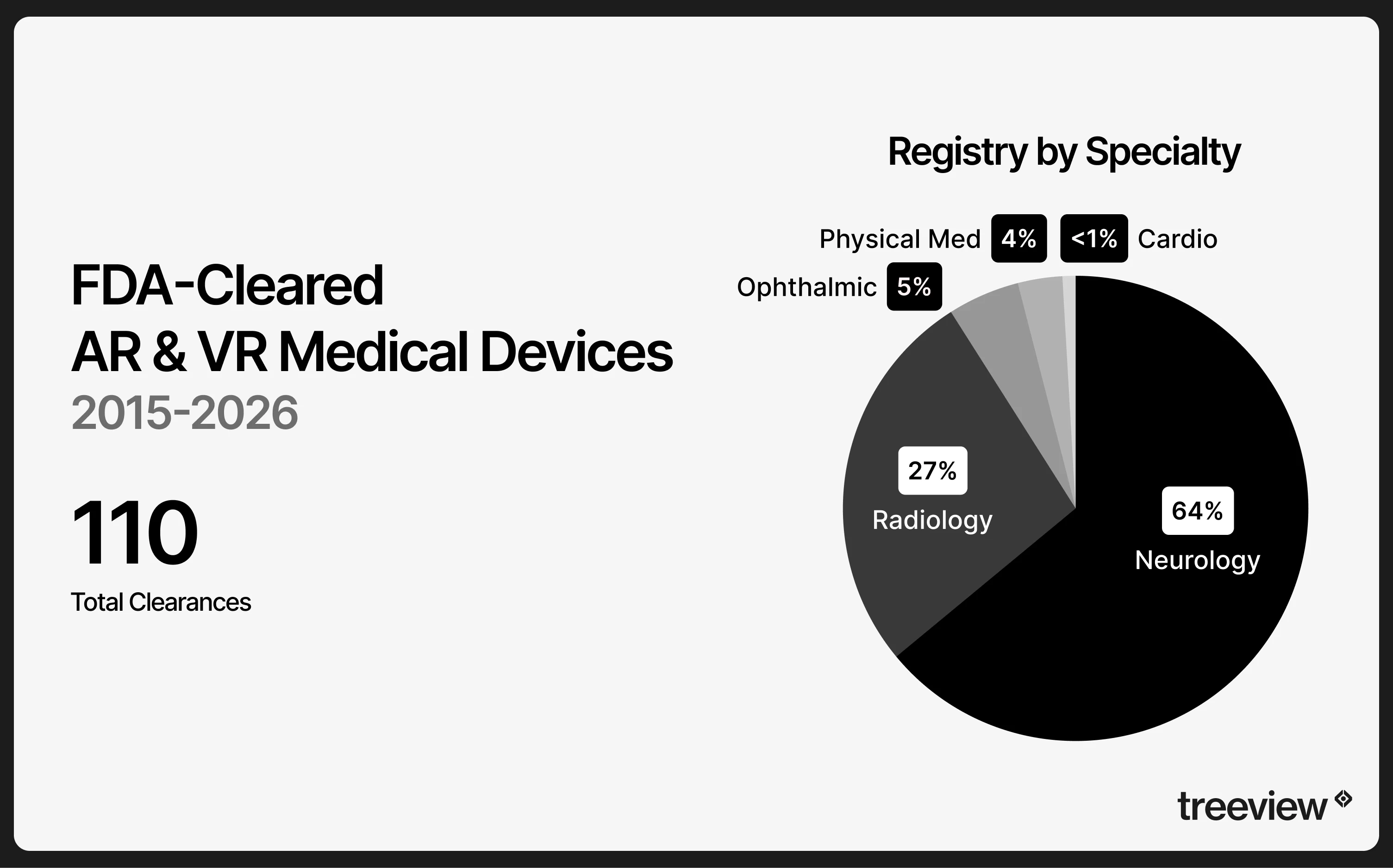

FDA-Cleared AR and VR Medical Devices (2015-2026)

The FDA has cleared or authorized 110 AR and VR medical devices since 2015, spanning surgical navigation, radiology visualization, therapeutic VR, ophthalmic treatment, and physical medicine rehabilitation. Two devices received De Novo authorization, the highest regulatory bar in the registry, authorizing VR as a standalone therapeutic intervention rather than a visualization or navigation tool.

The full registry is available at the FDA Digital Health Center of Excellence.

Regulatory Pathway: 510(k) vs. De Novo

The majority of cleared AR and VR medical devices received 510(k) clearance, which requires demonstrating substantial equivalence to a legally marketed predicate device. Two devices received De Novo authorization, a higher regulatory bar applied to novel devices with no predicate. De Novo authorization establishes a new device type and can serve as the predicate for future 510(k) submissions.

Both De Novo authorizations in the FDA AR/VR registry are therapeutic VR devices:

EaseVRx (AppliedVR, November 2021): the first FDA-authorized prescription VR therapy, indicated as an adjunct treatment for chronic lower back pain. Now marketed as RelieVRx.

Luminopia One (Luminopia, October 2021): FDA-authorized VR treatment for amblyopia (lazy eye) in children aged 4-7, used in conjunction with optical correction.

Most Active Companies by FDA Clearance Volume

Company | Cleared Devices | Primary Application |

|---|---|---|

Medacta International | 7 clearances | AR surgical navigation: spine, knee, shoulder, RSA platforms (NextAR series) |

Augmedics | 5 clearances | AR spine surgery navigation (xvision Spine system) |

Surgical Theater | 5 clearances | Patient-specific VR/AR surgical planning and navigation (SNAP, SpineAR) |

Pixee Medical | 4 clearances | AR knee replacement navigation (Knee+) |

Brainlab AG | 3 clearances | Mixed reality radiology visualization and spine navigation |

MR Surgical Solutions | 3 clearances (2025 only) | AR shoulder navigation (OptiVu Shoulder) |

Medivis | 3 clearances | AR surgical navigation: SurgicalAR, spine, NeuroAlign |

Repeat clearances from Augmedics, Medacta International, and Surgical Theater reflect iterative software updates submitted as new 510(k)s, a common regulatory strategy for software-driven medical devices.

Devices by Medical Specialty

Specialty | Share of Registry | Primary Device Types |

|---|---|---|

Neurology (spine, brain, orthopedic) | ~64% | AR surgical navigation, VR cognitive assessment, spine planning |

Radiology | ~27% | AR/MR imaging visualization, 3D anatomy rendering |

Ophthalmic | ~5% | VR amblyopia treatment (Luminopia), digital prism correction (Apple) |

Physical Medicine / Rehab | ~4% | VR motor rehabilitation (MindMotion, REAL Immersive System) |

Cardiovascular | <1% | AR cardiac monitoring (VivaQuant) |

Notable Cleared Devices

The nine devices below represent the most significant AR and VR clearances in the FDA registry by regulatory standing, clinical reach or commercial deployment. Two carry De Novo authorization, a designation reserved for novel device types with no predicate, and the highest regulatory bar in the registry. The remaining seven received 510(k) clearance. Clearance dates, indications and key clinical facts are included for each.

Device | Company | Pathway | Cleared | Indication | Key Fact |

|---|---|---|---|---|---|

xvision Spine System | Augmedics | 510(k) x5 | 2019, 2021, 2022, 2024, 2025 | AR intraoperative navigation for spine surgery | Most repeatedly cleared AR surgical navigation device in the registry |

RelieVRx / EaseVRx | AppliedVR | De Novo + 510(k) x2 | Nov 2021, Dec 2024, Aug 2025 | Adjunct treatment for chronic lower back pain | First FDA-authorized prescription VR therapy; $200,000/month documented medication cost savings |

SpineAR SNAP / SyncAR Spine | Surgical Theater | 510(k) x3 | Sep 2022, Dec 2024, Sep 2025 | AR spine surgical navigation | Built on patient-specific MRI and CT imaging pipeline |

Luminopia One | Luminopia | De Novo + 510(k) | Oct 2021, Oct 2023 | VR treatment for pediatric amblyopia (ages 4-7) | Only FDA-authorized VR treatment for an ophthalmic condition |

Digital Prism Correction Feature | Apple Inc. | 510(k) x2 | Oct 2024, Jun 2025 | Ophthalmic accommodation for Apple Vision Pro users | First FDA clearance for an Apple Vision Pro feature |

CommandEP / SentEP | SentiAR | 510(k) x2 | Sep 2020 (SentEP), Jul 2023 (CommandEP) | Holographic AR display for cardiac electrophysiology | Projects real-time 3D cardiac anatomy and catheter position during ablation |

REAL Immersive System | Penumbra | 510(k) | Mar 2019 | Upper extremity VR rehabilitation post-stroke | One of the earliest FDA-cleared VR rehabilitation systems |

Smileyscope System | Smileyscope | 510(k) | Sep 2023 | Pediatric procedural pain distraction (venipuncture, IV) | VR distraction without pharmacologic intervention |

inVisionOS | PrecisionOS | 510(k) | Nov 2021 | VR orthopedic surgical training | One of few surgical simulation platforms to pursue FDA clearance |

What the FDA Registry Tells Us

AR navigation dominates therapeutic VR in clearance volume: Of the 110 cleared devices, approximately 90 are AR surgical navigation or imaging visualization tools. Therapeutic VR devices represent roughly 10% of clearances by count but hold the highest public profile, driven by the De Novo authorizations.

Clearance activity is accelerating: The FDA registry logged 12 clearances in all of 2024, and 15 clearances in the first ten months of 2025 alone.

Spine surgery is the dominant clinical application: Roughly 40% of all cleared devices are spine-specific AR navigation systems, reflecting both procedural complexity and the commercial activity of orthopedic device companies investing in AR-assisted surgical tools.

VR and AR in Healthcare: Clinical Trials

Treeview analyzed 2,089 unique VR and AR healthcare studies registered on ClinicalTrials.gov as of May 2026. The figures below are drawn directly from downloaded ClinicalTrials.gov data.

Metric | Count |

|---|---|

Total registered VR/AR studies | 2,089 |

VR-specific studies | 1,493 |

AR-specific studies | 112 |

Completed | 1,891 |

Active (data collection ongoing) | 116 |

Terminated | 82 (3.9%) |

Studies including pediatric patients | 548 |

Pain is the largest condition cluster with 361 studies, once all pain-related terms are counted together: chronic pain, postoperative pain, acute pain, burn pain and procedural pain. Anxiety follows at 297 studies, then stroke (163), stress (75), cancer (65), cerebral palsy (55), fear (55), multiple sclerosis (37), depression (33) and chronic pain (32).

The 116 active studies show where current institutional investment is flowing: pain (26), mental health and anxiety (24), rehabilitation and neurology (19), training and medical education (6), surgical (4) and cancer and oncology (3).

Pediatric research is concentrated in anxiety (110 studies involving children, 37% of all anxiety studies), pain (103 studies, 29%) and cerebral palsy (54 of 55 studies, almost entirely a pediatric condition in this dataset).

CMS Reimbursement: What Has Already Changed

CMS activated the first Medicare reimbursement codes for FDA-cleared digital therapeutics in January 2025. Further coverage changes followed through 2026.

January 2025: The Centers for Medicare & Medicaid Services (CMS) activated three new reimbursement codes for FDA-cleared Digital Mental Health Treatment (DMHT) devices, the first Medicare reimbursement pathway for software-based therapeutics in US history. Coverage applies when a billing practitioner diagnoses the patient with a mental health condition and prescribes the DMHT device as part of an ongoing behavioral health treatment plan.

November 2025: CMS expanded the DMHT reimbursement framework to include digital therapeutics for ADHD, effective January 2026. The Digital Therapeutic Alliance called the original 2025 codes "the first acknowledgment of a pathway for reimbursement for a certain sector of digital therapeutic interventions." The Alliance noted they set "a precedent for Medicare coding, coverage and reimbursement that can be applied to additional therapeutic categories."

September 2025: Cigna Healthcare announced commercial insurance coverage for FDA-approved digital therapeutics, extending reimbursement access beyond Medicare to a major commercial payer.

April 2026: FDA and CMS jointly announced the RAPID pathway (Regulatory Alignment for Predictable and Immediate Device coverage), a mechanism to synchronize FDA clearance timelines with Medicare coverage determinations. RAPID targets breakthrough-designated devices, which include VR therapeutics. The pathway does not deliver automatic coverage, but it significantly shortens the lag between FDA authorization and Medicare eligibility.

RelieVRx (AppliedVR): CMS established an HCPCS code for the RelieVRx chronic lower back pain VR program, creating a formal Medicare coverage eligibility pathway. Final payment determination is pending a CMS HCPCS public meeting.

What Remains Unresolved

CMS reimbursement for VR therapeutics currently covers only a narrow slice: FDA-cleared digital mental health devices used in conjunction with an active behavioral health treatment plan, billed by a licensed prescriber. VR pain management, VR rehabilitation and VR surgical training are not yet covered under any Medicare reimbursement code. The RAPID pathway and DMHT expansion signal the direction of travel, but VR's biggest revenue opportunities in healthcare remain outside the reimbursement framework as of mid-2026.

Virtual Reality in Healthcare: Medical Training & Simulation

Virtual reality in medical training delivers simulation-based education in environments that would be dangerous, impractical or impossible to replicate in traditional settings. Surgical training is the highest-CAGR application in the healthcare VR market; patient care management holds the largest current revenue share.

The ACGME (Accreditation Council for Graduate Medical Education) now mandates simulation training for surgical residents in the United States, embedding virtual reality into the accreditation pathway for surgical programs.

VR in Medical Simulation

The global VR in medical simulation market reached $2.7 billion in 2022 and is projected to reach $29.6 billion by 2031 at a CAGR of 36.6% (DataM Intelligence).

Key adoption statistics:

77% of healthcare organizations have implemented or are planning to implement VR for training (Virti survey, 211 US healthcare workers, 2023).

70% of US hospitals use AR/VR tools specifically for training and surgical support.

65% of US medical professionals prefer VR-based learning for understanding complex procedures.

30% of universities worldwide now offer VR-based courses as of 2024.

Virtual reality medical training outcomes:

VR-trained medical students recorded 40% fewer errors compared to control groups in a peer-reviewed Vantari VR study (ScienceDirect).

VR-trained medical students completed a standard orthopedic procedure faster and with fewer redirections than traditionally trained peers (statistically significant, P < 0.05 and P = 0.05).

A 2025 meta-analysis of VR in nursing education found that immersive simulations consistently improved clinical decision-making in unpredictable, high-stress scenarios.

PwC's VR Soft Skills Study documented that VR learners are up to 4x faster to train than classroom learners and 275% more confident to apply skills learned after training.

Surgical Simulation

The global surgical simulation market reached $3.85 billion in 2025 and is projected to reach $15.31 billion by 2035 at a CAGR of 14.8% (Towards Healthcare). VR accounted for 38% of the surgical simulation market in 2025.

Leading surgical VR platforms in active clinical use:

Osso VR: Procedure-specific surgical training with AI-driven performance analytics.

PrecisionOS: Orthopedic surgical simulation matched to specific implants and instruments.

FundamentalVR: AI-assisted surgical skills training with real-time feedback.

Medicalholodeck: Multi-user medical VR for collaborative clinical training.

In 2025, Medivis launched a multicenter study to validate its XR90 Holographic Surgical Navigation system as an adjunct to standard imaging in percutaneous tumor biopsies.

Augmented Reality in Healthcare: AR-Guided Surgery & Surgical Navigation

Augmented reality development in healthcare surgery is increasingly integrated into navigation systems, overlaying real-time imaging data, anatomical models, and procedural guidance directly onto the surgeon's field of view.

The global surgical navigation systems market was estimated at $8.41 billion in 2024 and is projected to reach $35.68 billion by 2035 at a CAGR of 14.04%. The integration of AR, AI, and robotics is reshaping how complex surgeries are planned and executed.

Specific adoption signals:

Mayo Clinic reports lower procedural complications when surgical residents practice on AR modules before entering the operating room.

Recent AR navigation prototypes add voice-controlled navigation, letting surgeons reposition virtual anatomy without touching screens, lowering infection risk and reducing cognitive workload.

In 2025, Kauvery Hospital introduced Chennai's first O-ARM with AI-powered Navigation System for complex brain, spine, and orthopedic surgeries.

Intuitive Surgical's da Vinci robotic systems reached an installed base of 8,606 units globally, facilitating approximately 2.286 million procedures in 2023; da Vinci's integration with surgical AR navigation is a direct growth driver.

Augmented reality in healthcare hardware (2025): Hardware composed 54.72% of AR in healthcare market revenue in 2025. The AR in healthcare services segment is the fastest-growing component, expanding at a 27.90% CAGR through 2031, reflecting hospital demand for turnkey workflow integration, staff certification, and ongoing support.

Virtual Reality for Pain Management

VR-based pain management is one of the most clinically validated use cases for virtual reality in healthcare. VR reduces pain intensity by 35-50% in burn wound care procedures, reduces fear and anxiety in pediatric patients undergoing needle procedures, and has documented $200,000 in monthly cost savings through reduced medication requirements.

Key clinical outcomes:

VR interventions during burn wound care demonstrated a 35-50% reduction in reported pain intensity, consistently outperforming standard distraction methods (NIH/PMC umbrella review).

EaseVRx (now RelieVRx, AppliedVR) clinical deployments documented $200,000 in monthly cost savings through reduced medication requirements.

A systematic review in the Journal of Clinical Medicine (2021) confirmed statistically significant reductions in pain, fear, and anxiety in pediatric patients undergoing needle-related procedures.

A 2025 scoping review in the Journal of Medical Internet Research found VR effective across fibromyalgia, complex regional pain syndrome (CRPS), neuropathic pain, and chronic neck and low-back pain.

Immersive VR is more effective than non-immersive VR: in a systematic review, 8 of 10 immersive VR studies reported significant pain reduction, vs. 4 of 7 non-immersive studies.

Opioid reduction context: The CDC recommends maximizing non-pharmacologic therapies amid the ongoing opioid overdose crisis. VR offers a low-risk, non-addictive intervention with low incidence of side effects (dizziness, headache, nausea, eye strain) and potential to reduce medication reliance and associated healthcare costs.

VR in Mental Health & Behavioral Therapy

Mental health therapy is the fastest-growing application segment within the AR and VR in healthcare market by CAGR. VR mental health therapy is active across PTSD, anxiety disorders, specific phobias, schizophrenia, depression, addiction, phantom limb pain, and autism spectrum disorder social skills training.

Market context:

The VR mental health therapy segment is projected to be the fastest growing within the overall healthcare AR/VR market through the forecast period (2025-2033+).

In 2025, Wundrsight raised seed funding to expand VR-based mental health hospital and clinical partnerships in India.

In 2025, Strolll raised £10.35 million to advance AR glasses for patients with neurological disorders including Parkinson's disease, stroke, and multiple sclerosis.

VR in Healthcare: Rehabilitation

Virtual reality in healthcare rehabilitation enables repetitive task training with real-time feedback in stroke recovery, orthopedic rehabilitation, and neurological motor skill retraining. VR increases patient engagement compared to conventional physiotherapy and enables clinicians to track progress metrics remotely.

Key rehabilitation use cases:

Stroke rehabilitation: Virtual reality environments enable repetitive task training with real-time feedback, increasing engagement compared to conventional physiotherapy.

Orthopedic recovery: VR-guided movement programs help patients regain range of motion post-surgery, with clinician oversight of progress metrics.

Neurological disorders: Strolll AR glasses are designed to assist gait and movement for patients with Parkinson's disease and multiple sclerosis, providing real-time environmental cues.

The virtual training and simulation market was estimated at $449.9 billion in 2024 and is projected to reach $844.2 billion by 2030 at an 11.1% CAGR (ScienceSoft).

Investment & Funding

Healthcare AR and VR attracted significant investment across platforms, hardware and government programs in 2025. Key rounds:

XPANCEO raised $250 million in Series A funding (July 2025) to develop an all-in-one XR smart contact lens targeting healthcare and consumer markets.

Strolll raised £10.35 million (March 2025) for AR glasses targeting neurological disorder patients.

XRHealth positioned itself as the largest AI-driven therapeutic VR platform worldwide following a strategic acquisition in 2025.

The UK government allocated £12 million across 11 projects through its Addiction Healthcare Goals programme to develop XR-assisted addiction treatment solutions.

Adoption Drivers & Barriers

VR adoption in healthcare is accelerating due to regulatory mandates, growing clinical evidence, and improving hardware accessibility. The primary barriers are data privacy concerns, skills gaps, and reimbursement uncertainty.

What Is Driving Adoption

Staff shortages: Global healthcare systems face critical clinician supply gaps. VR training scales instruction without proportional headcount or physical facility cost.

Regulatory mandates: ACGME simulation requirements in the United States are embedding virtual reality into surgical residency programs by regulatory necessity.

Clinical evidence: Peer-reviewed outcomes data for VR in surgery, pain management, and rehabilitation is growing rapidly, reducing adoption risk for hospital procurement committees.

AI integration: VR platforms are adding AI-driven feedback, performance analytics, and adaptive simulation, making healthcare VR tools significantly more valuable than static e-learning alternatives.

Hardware accessibility: Meta Quest's enterprise pivot and Apple Vision Pro's enterprise-first posture have legitimized XR hardware within clinical IT procurement. For an overview of the current headset landscape, see Meta for Work's analysis of VR healthcare technology.

What Is Slowing Adoption

Data privacy and security: Approximately 62% of healthcare organizations cite data privacy concerns as a primary barrier.

Skills gap: Around 58% of providers report a lack of trained staff to operate and maintain VR systems.

Integration complexity: Roughly 55% identify integration with existing EHR, imaging, and workflow systems as a significant challenge.

Reimbursement uncertainty: CMS reimbursement frameworks for VR-delivered care remain limited, creating budget justification challenges for healthcare CFOs.

Capital cost: Hardware remains a non-trivial line item, particularly for health systems outside North America and Western Europe.

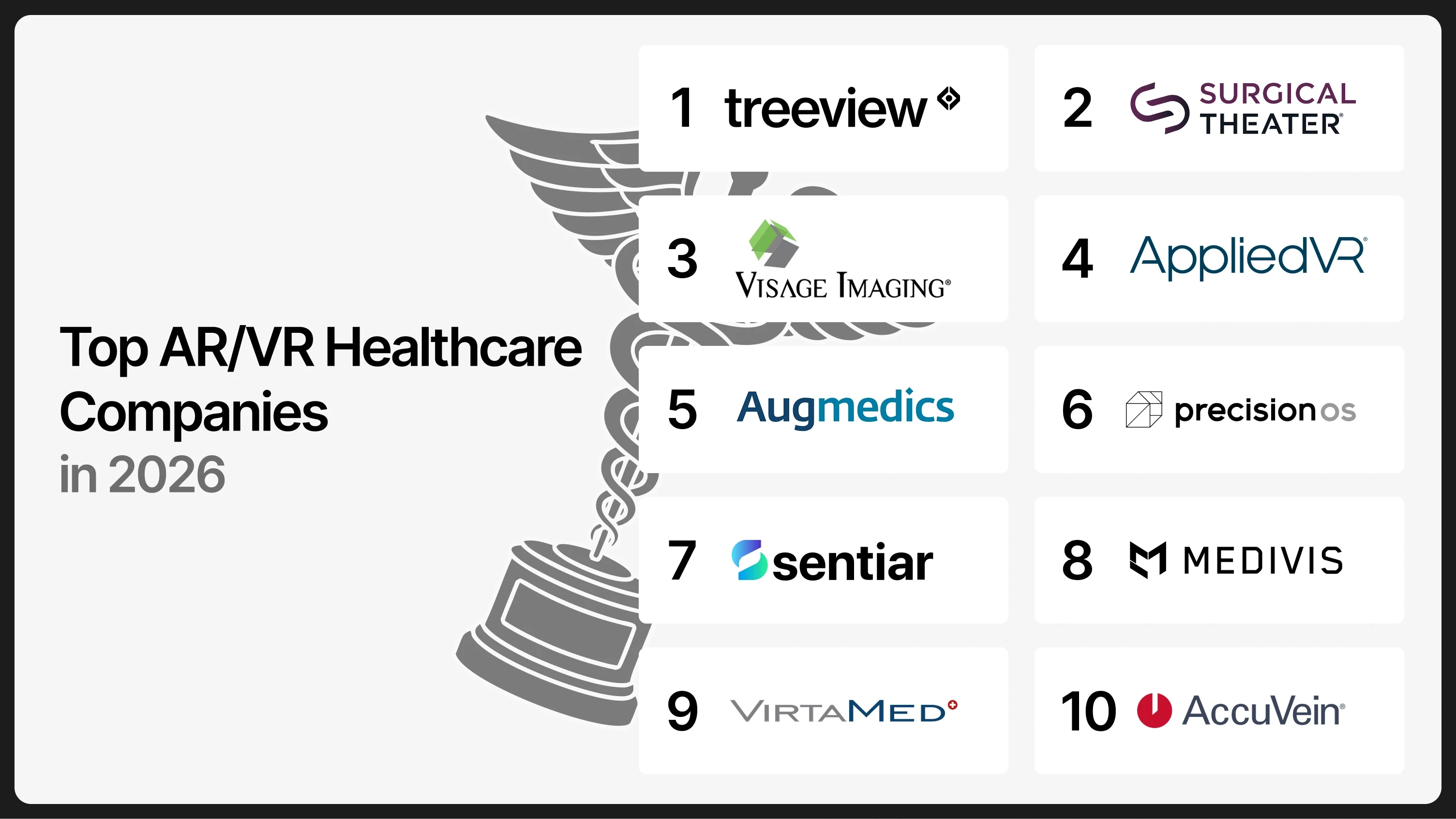

Key Companies in Healthcare AR and VR

The following rankings are drawn from Treeview's guide to the top VR, AR, MR and XR companies for healthcare, where full company profiles, use case breakdowns and selection criteria are documented. For specific deployment examples, see 65+ real-world VR and AR in healthcare examples.

Rank | Company | Best For |

|---|---|---|

1 | Treeview | Custom enterprise AR/VR/MR: surgical training, medical device visualization, pharma field force, surgical planning, cardiovascular simulation |

2 | Surgical Theater | Patient-specific VR/AR surgical rehearsal for neurosurgery and complex procedures |

3 | Visage Imaging | Apple Vision Pro medical imaging: spatial, immersive DICOM navigation for radiology and cardiology |

4 | AppliedVR | FDA-authorized prescription VR for chronic pain management |

5 | Augmedics | FDA-cleared AR intraoperative navigation for spine surgery |

6 | PrecisionOS | VR surgical training for orthopedic implant and instrument procedures |

7 | SentiAR | Holographic AR display for cardiac electrophysiology procedures |

8 | Medivis | Surgical AR software for pre-operative anatomy visualization |

9 | VirtaMed | High-fidelity VR medical simulators for laparoscopy, arthroscopy, and urology |

10 | AccuVein | AR vascular projection for IV access and blood draw support |

Company Profiles

Treeview is a senior-only enterprise spatial computing studio (New York and Montevideo, founded 2016) building custom VR, AR, and MR applications for healthcare and life sciences clients. Treeview client work includes the Micra XR Trainer (VR pacemaker implantation simulation for Medtronic), CardioCompass (cardiovascular health simulation for Daiichi Sankyo), and the Inviewer spatial health education platform.

Surgical Theater builds patient-specific surgical rehearsal environments from each patient's MRI, CT, and DTI imaging. Surgical Theater operates across pre-operative planning, intraoperative AR navigation, and patient education, with active deployments at major US hospital systems and Rambam Healthcare Medical Center in Israel.

Visage Imaging builds medical imaging software with a native Apple Vision Pro application, Visage Ease VP, that brings spatial and immersive DICOM navigation to radiologists and clinicians. Visage Ease VP leverages Apple Silicon and a cinematic rendering engine to deliver volume-rendered imaging in immersive space, using eyes, hands and voice for navigation.

AppliedVR (Los Angeles) holds the most significant regulatory milestone in medical VR: RelieVRx, the first FDA-authorized prescription VR therapy, authorized in 2023 for adjunct treatment of chronic lower back pain. RelieVRx clinical deployments have documented $200,000 in monthly cost savings and a 50% reduction in patient pain scores.

Augmedics developed the xvision Spine System, an AR headset that overlays real-time holographic guidance on the patient's spine during surgery. Augmedics' xvision Spine System is FDA-cleared and enables surgeons to see anatomical structures without fluoroscopy or breaking sterile field.

PrecisionOS (Vancouver) builds VR surgical training for orthopedic implant and instrument procedures. PrecisionOS simulations match the exact instruments surgeons will use in surgery. PrecisionOS is used by major orthopedic device companies for field force and surgeon training.

SentiAR (St. Louis) displays real-time holographic anatomical data during cardiac electrophysiology procedures via Microsoft HoloLens 2. SentiAR enables more precise catheter navigation without requiring the cardiologist to look away from the patient.

Medivis (New York) builds surgical AR software for pre-operative anatomy visualization and intraoperative guidance. Medivis's SurgicalAR platform overlays patient-specific CT and MRI data onto the patient in the OR via AR headset. Medivis's multicenter XR90 Holographic Surgical Navigation study (launched 2025) is evaluating the platform as an adjunct to standard imaging in percutaneous tumor biopsies.

VirtaMed (Zurich and Chicago) produces high-fidelity VR medical simulators for laparoscopy, arthroscopy, hysteroscopy, and urology. VirtaMed simulators use physical instrument handles connected to real-time haptic feedback systems, providing tactile as well as visual simulation.

AccuVein (Cold Spring Harbor, NY) uses AR projection to display a real-time map of a patient's veins on the surface of their skin without contact. AccuVein has been used on over 40 million patients across more than 3,000 healthcare facilities worldwide.

Treeview Perspective: What We See Building Healthcare VR

Treeview has built VR and AR applications for enterprise healthcare clients including Medtronic and Daiichi Sankyo since 2016. The observations below come from client discovery calls, project scopes and procurement conversations, not market research reports.

Is Virtual Reality adoption in Healthcare still about proving it works?

No. Two years ago, healthcare enterprise conversations started with "does virtual reality actually work for training?" That question is settled. Clinical outcomes data, ACGME mandates and peer institution deployments have answered it. The question now is "how do we integrate this into existing workflows and make the business case stick internally?" That is where most implementations stall.

Why is Meta Quest winning in Clinical VR Training over Tethered AR?

Meta Quest dominates enterprise healthcare VR training because it removes setup friction. Tethered AR systems like Microsoft HoloLens 2 and Magic Leap require IT configuration, have higher per-device cost and are more fragile in high-turnover clinical environments. For surgical simulation and clinical education, the fidelity tradeoff of a standalone headset is worth the operational simplicity. The exception is intraoperative AR guidance, where optical see-through and hands-free operation justify the complexity.

What makes a Healthcare VR ROI Case actually get approved?

Healthcare VR projects most likely to receive internal sign-off are scoped to a specific procedure or competency, with a measurable outcome tied to a cost line the CFO already cares about: OR time, training cohort throughput, complication rates or credentialing cycle time. Broad "immersive learning" proposals with diffuse ROI claims do not make it past procurement.

Which Healthcare Organizations are the biggest VR Buyers that nobody talks about?

Pharmaceutical and medical device companies. Medtronic, Stryker and Daiichi Sankyo use VR and AR for healthcare professional (HCP) education, sales rep training and product launch content at scale. This use case is not clinical care and does not appear prominently in market reports, but it drives meaningful XR development volume at the enterprise level.

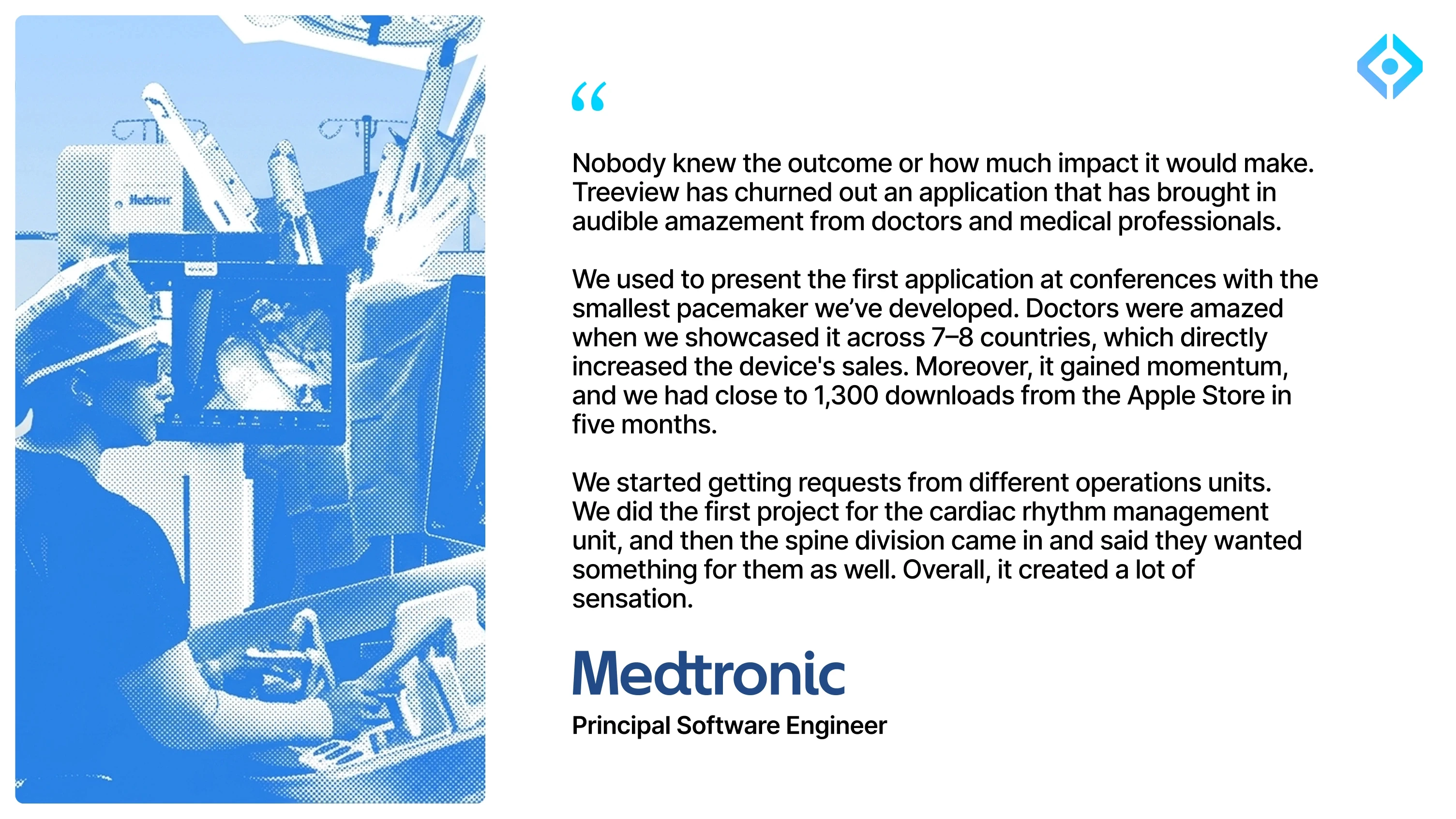

The Medtronic engagement is a direct example. Treeview built the Micra XR Trainer, a VR application for Medtronic's smallest pacemaker, and the results went well beyond internal training. A Medtronic Principal Software Engineer described the outcome on Clutch:

"Nobody knew the outcome or how much impact it would make. Treeview has churned out an application that has brought in audible amazement from doctors and medical professionals.

We used to present the first application at conferences with the smallest pacemaker we've developed. Doctors were amazed when we showcased it across 7–8 countries, which directly increased the device's sales. Moreover, it gained momentum, and we had close to 1,300 downloads from the Apple Store in five months.

We started getting requests from different operations units. We did the first project for the cardiac rhythm management unit, and then the spine division came in and said they wanted something for them as well. Overall, it created a lot of sensation."

— Principal Software Engineer, Medtronic (Clutch)

What is the longest lead-time item in a Healthcare VR Deployment?

HIPAA compliance review, not the technical build. HIPAA compliance review, IT security approval and MDM provisioning for headsets in clinical environments routinely add 3–6 months to deployment timelines. Studios that come to procurement with this process pre-mapped have a significant advantage over those treating it as an afterthought.

Where Virtual Reality in Healthcare Stands in 2026

The healthcare VR and AR market in 2026 is transitioning from early majority to mainstream adoption. The clinical evidence base has shifted procurement conversations from "does this work?" to "how do we integrate this?" The regulatory environment is codifying virtual reality into training standards. The hardware ecosystem, led by mixed reality headsets including Meta Quest and Apple Vision Pro, has delivered devices meeting clinical-grade requirements for fidelity and reliability.

Three developments will define the next phase:

Reimbursement: The pathway is open. CMS activated the first Medicare reimbursement codes for FDA-cleared digital mental health therapeutics in January 2025. Cigna extended commercial coverage in September 2025. The FDA and CMS jointly launched the RAPID breakthrough device coverage pathway in April 2026. RelieVRx holds an HCPCS code with Medicare coverage eligibility pending final payment determination. The coverage framework currently applies to digital mental health devices only. VR pain management, rehabilitation and surgical training remain outside Medicare reimbursement as of mid-2026, but the regulatory and payer infrastructure is now in place.

AI-VR convergence: The most significant near-term product development is not better headsets. It is AI-driven simulation that adapts in real time to trainee performance, generates novel patient scenarios, and integrates with clinical competency frameworks. The platforms building this layer, including FundamentalVR, Osso VR, and XRHealth, will capture disproportionate value.

Enterprise standardization: Healthcare systems are moving from single-department pilots to system-wide procurement. This requires VR and AR development vendors to demonstrate EHR interoperability, HIPAA compliance, and ROI metrics that finance departments can validate.

Frequently Asked Questions: Virtual Reality & Augmented Reality in Healthcare

Q1. What is the size of the AR and VR in healthcare market in 2025?

The global VR in healthcare market reached $5.62 billion in 2025 and is projected to reach $7.58 billion by end of 2026, growing to $66.91 billion by 2034 at a 31.3% CAGR (Fortune Business Insights). The augmented reality in healthcare segment is growing at 33.9% CAGR, the fastest vertical growth rate in the XR industry.

Q2. What is the fastest-growing segment within healthcare VR and AR?

The mental health therapy segment is projected to be the fastest-growing application within the healthcare AR/VR market by CAGR, followed closely by surgical training and AR-guided procedures.

Q3. How effective is virtual reality for pain management?

Clinical studies show VR reduces pain intensity by 35-50% during burn wound care procedures. EaseVRx (now RelieVRx) clinical deployments have documented $200,000 in monthly cost savings and a 50% reduction in patient pain scores through reduced medication requirements. VR is effective across chronic pain conditions including fibromyalgia, CRPS, neuropathic pain, and low-back pain.

Q4. How widely is VR adopted in hospitals?

Approximately 40% of healthcare providers globally use virtual reality for patient treatment or staff training. In the US specifically, 70% of hospitals report using AR/VR tools for training and surgical support. A 2023 Virti survey found 77% of healthcare organizations have implemented or are planning to implement VR for training.

Q5. What are the biggest barriers to virtual reality adoption in healthcare?

The primary barriers are data privacy concerns (cited by ~62% of organizations), skills gaps (~58%), EHR and workflow integration complexity (~55%), and reimbursement uncertainty. Capital cost remains a barrier for smaller health systems outside North America and Western Europe.

Q6. What hardware is used for virtual reality in clinical settings?

The most widely deployed platforms include Meta Quest (dominant in VR training and simulation, 53% standalone headset market share), Microsoft HoloLens 2 (surgical navigation and AR overlays, 60% of published HoloLens 2 clinical studies focus on surgical navigation), Apple Vision Pro (medical imaging review, clinical education), and Varjo XR-4 (high-fidelity surgical simulation at 51 PPD display resolution).

Q7. What is XRHealth?

XRHealth is the largest AI-driven therapeutic virtual reality platform globally as of 2025, following a strategic acquisition. XRHealth delivers clinically validated VR therapies across rehabilitation, cognitive therapy, and pain management, with real-time clinical data reporting integrated into care workflows.

Q8. How is virtual reality used in surgical training?

Surgical VR training platforms including Osso VR, PrecisionOS, and FundamentalVR deliver high-fidelity procedural simulation with haptic feedback, allowing surgeons and residents to rehearse procedures before entering the operating room. VR-trained medical students recorded 40% fewer errors compared to control groups in a peer-reviewed Vantari VR study.

Q9. What is the outlook for virtual reality in mental health?

VR-based mental health therapy is the fastest-growing application in healthcare VR by CAGR. Active treatment areas include PTSD, anxiety disorders, phobias, depression, and addiction. The UK government has allocated £12 million to develop VR-assisted addiction treatment through its Addiction Healthcare Goals programme. Multiple clinical trials are underway in Europe and North America.

Q10. Which companies lead in healthcare VR and AR?

Leading companies in healthcare VR and AR include Treeview (enterprise XR development), XRHealth (therapeutic VR platform), Osso VR, FundamentalVR, PrecisionOS, Medtronic, Siemens Healthineers, GE Healthcare, CAE Healthcare, Medivis, and Varjo. Hardware manufacturers with significant healthcare presence include Meta, Apple, and Microsoft.

Sources and Methodology

Market size figures in this report are drawn from Fortune Business Insights, Grand View Research, MarketDataForecast, DataM Intelligence, Towards Healthcare, Global Growth Insights, Mordor Intelligence, and Verified Market Research. Because these firms differ in scope definitions (some include only hardware, others include software, services and adjacent markets), figures are cited with their source and should be treated as directional rather than definitive.

Clinical outcomes data is sourced from peer-reviewed journals including PubMed/PMC, JMIR, Frontiers in Medicine and ASRA. Adoption statistics are drawn from industry surveys cited by firm. The Treeview Perspective section reflects direct observations from Treeview's engagement with enterprise healthcare clients and is not sourced from third-party research.

Primary sources:

Fortune Business Insights: Virtual Reality in Healthcare Market, 2025-2034

Grand View Research: Virtual Reality in Healthcare Market Size, Share & Trends, 2025-2030

Verified Market Research: Virtual Reality in Healthcare Market Report, 2025-2033

MarketDataForecast: AR & VR in Healthcare Market Size & Growth Report, 2033

DataM Intelligence: VR/AR Technology for Healthcare Market, May 2026

Global Growth Insights: AR & VR in Healthcare Market, April 2026

DataM Intelligence: VR in Medical Simulation Market, February 2026

GlobeNewswire: Surgical Navigation Systems Market 2025-2035, January 2025

HBR / Gideon Blumstein: Research: How Virtual Reality Can Help Train Surgeons, 2019

PRNewswire / Virti: 77% of Healthcare Organizations Have Implemented VR for Training, 2023

NIH/PMC: Virtual reality for pain management: an umbrella review

NIH/PMC: Harnessing virtual reality in pain management: a call for standardization

JMIR: Virtual Reality Interventions and Chronic Pain: Scoping Review, 2025

NIH/PMC: Effectiveness of VR-Based Interventions for Managing Chronic Pain

NIH/PMC: Journal of Clinical Medicine: VR for Needle-Related Procedural Pain in Pediatrics, 2021

ScienceDirect / Vantari VR: VR Training and Surgical Error Reduction

Meta for Work: How VR healthcare technology is changing the field

ASRA: Virtual Reality in Pain Management & Rehabilitation: An Update, 2024

Intel Market Research: Healthcare AR & VR Glasses Market Outlook 2026-2034

360iResearch: Healthcare AR & VR Glasses Market Size & Share 2026-2032

PubMed: Smart glasses in spinal surgery in low- and middle-income countries, East Africa study

ClinicalTrials.gov: Smart Glasses in Emergency Medicine, Sir Run Run Shaw Hospital

LBMC: Hospitals Should Ban Meta Ray-Ban Smart Glasses (HIPAA analysis), 2025

MDPI Sensors / Palumbo: Microsoft HoloLens 2 in Medical and Healthcare Context, 2022

Fast Company: Apple wants Vision Pro to be a medical hub, 2024

ClinicalTrials.gov: US National Library of Medicine clinical trials registry (Treeview dataset analysis, May 2026)

HealthLeaders Media: CMS Advances Virtual Care, Digital Health Coverage in Proposed 2025 PFS

TechTarget: CMS Establishes Reimbursement Pathway for Virtual Reality Program (RelieVRx HCPCS code)

McDermott+: Digital health policies in the CY 2026 PFS proposed rule, July 2025