TL;DR - Key XR Market Statistics

Metric | Value |

|---|---|

XR Market Value 2025 | $20.43B |

Projected XR Market 2030 | $85.56B |

XR Device Sales 2025 | 14.5 Million |

Fortune 500 Companies Using XR | >75% |

Global XR Users by 2029 | 3.7 Billion |

Feel free to read along or jump to the section that sparks your interest:

The extended reality (XR) market is entering a new phase. After years of being defined by Virtual Reality headsets, the industry's center of gravity has shifted toward lightweight, AI-enabled wearables that look like ordinary glasses.

In 2025, the XR market shipped 14.5 million devices globally, a 41.6% increase over 2024. That growth was not distributed evenly. Smart glasses drove almost all of it, while standalone VR and mixed reality headsets contracted in the first half of the year, down 14% year-over-year per Counterpoint Research, before recovering in H2. For the first time, smart glasses represented roughly half of all XR shipments worldwide, up from around 25% in 2024.

This report tracks unit sales, revenue and platform adoption across 18 XR devices.

Key Numbers at a Glance

The table below covers the major platforms tracked in this report. Lifetime units represent total hardware sold through Q4 2025. Monthly Active Users (MAU) figures are estimates derived from platform engagement data where available.

Platform | Lifetime Units | 2025 Units | YoY | MAU (est.) |

|---|---|---|---|---|

XR Market Total | 49.6M | 14.5M | +41.6% | — |

Meta Quest | 26.76M | 2.3M | -10% est. | 8.5M |

Ray-Ban Meta | 8.9M | 6.5M | +225% est. | 4M |

PSVR1 + PSVR2 | 8.7M | 1.3M est. | +63% | 1.5M |

Pico XR | 2.1M | 225K | +13% | 500K |

XREAL | 1.0M | 325K | +63% | 425K |

Apple Vision Pro | 475K | 85K | -78% | 275K |

Oakley Meta | 500K | 500K | New | — |

Amazon Echo Frames | 450K | 150K | Flat | — |

Valve Index | 240K | 30K | Declining | 180K |

Samsung Galaxy XR | 70K | 40K | New | — |

Varjo XR-4 | 5K | 2K | Flat | — |

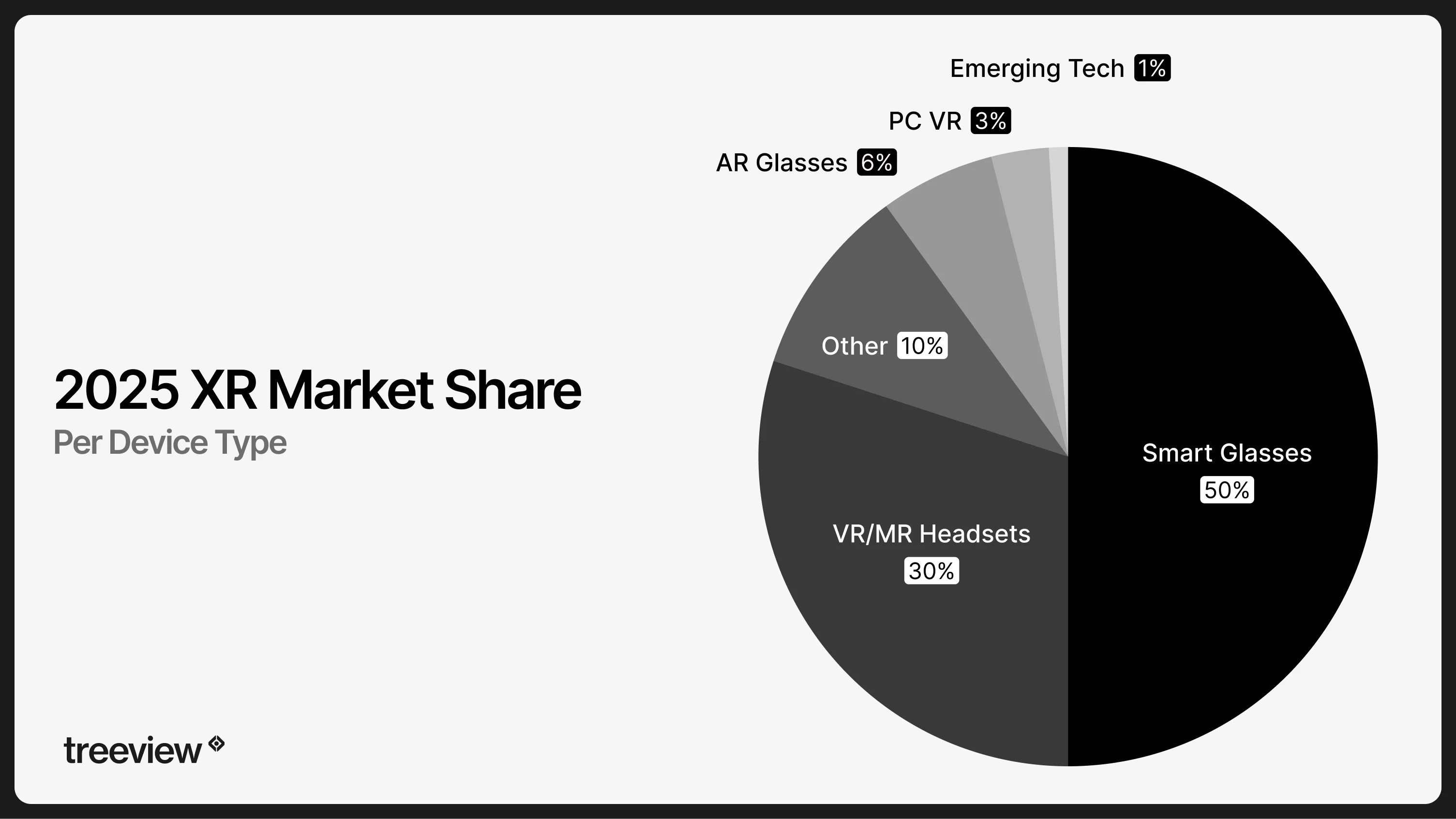

2025 XR Hardware Shipments by Segment

XR hardware spans six distinct categories that are frequently conflated. The most important distinction is between devices with an optical display (Augmented Reality glasses and VR/MR headsets) and devices without one, like smart glasses. For a deeper dive into the differences of each segment, we recommend reading the following blog posts: Difference Between AR/VR and Spatial Computing, Augmented Reality Guide, Virtual Reality Guide and Mixed Reality Guide.

Segment | What it is | 2025 Units | Share | Key Devices |

|---|---|---|---|---|

Smart Glasses (AI/camera) | Camera + AI, no display. Worn all day. | 7.25M | 50% | Ray-Ban Meta Gen 2, Oakley Meta HSTN, Amazon Echo Frames |

Standalone VR/MR Headsets | Self-contained 6DoF. No PC required. | 4.3M | 30% | Meta Quest 3S, Meta Quest 3, Pico 4 Ultra, Apple Vision Pro, Samsung Galaxy XR, Varjo XR-4 |

Other / Untracked | Optical see-through overlay (waveguide or birdbath). | 1.45M | 10% | Regional and untracked devices |

AR Display Glasses | Tethered to GPU. | 900K | 6% | XREAL One, RayNeo X3 Pro, VITURE One, Rokid Max 2, Meta Display |

PC VR Headsets | Ultra-premium tethered. | 450K | 3% | Valve Index, Bigscreen Beyond 2 |

Developer / Emerging | Sub-scale, dev-program or open hardware. | 50K | <1% | Snap Spectacles 2024, Brilliant Labs Frame, AjnaLens |

Total | 14.5M | 100% |

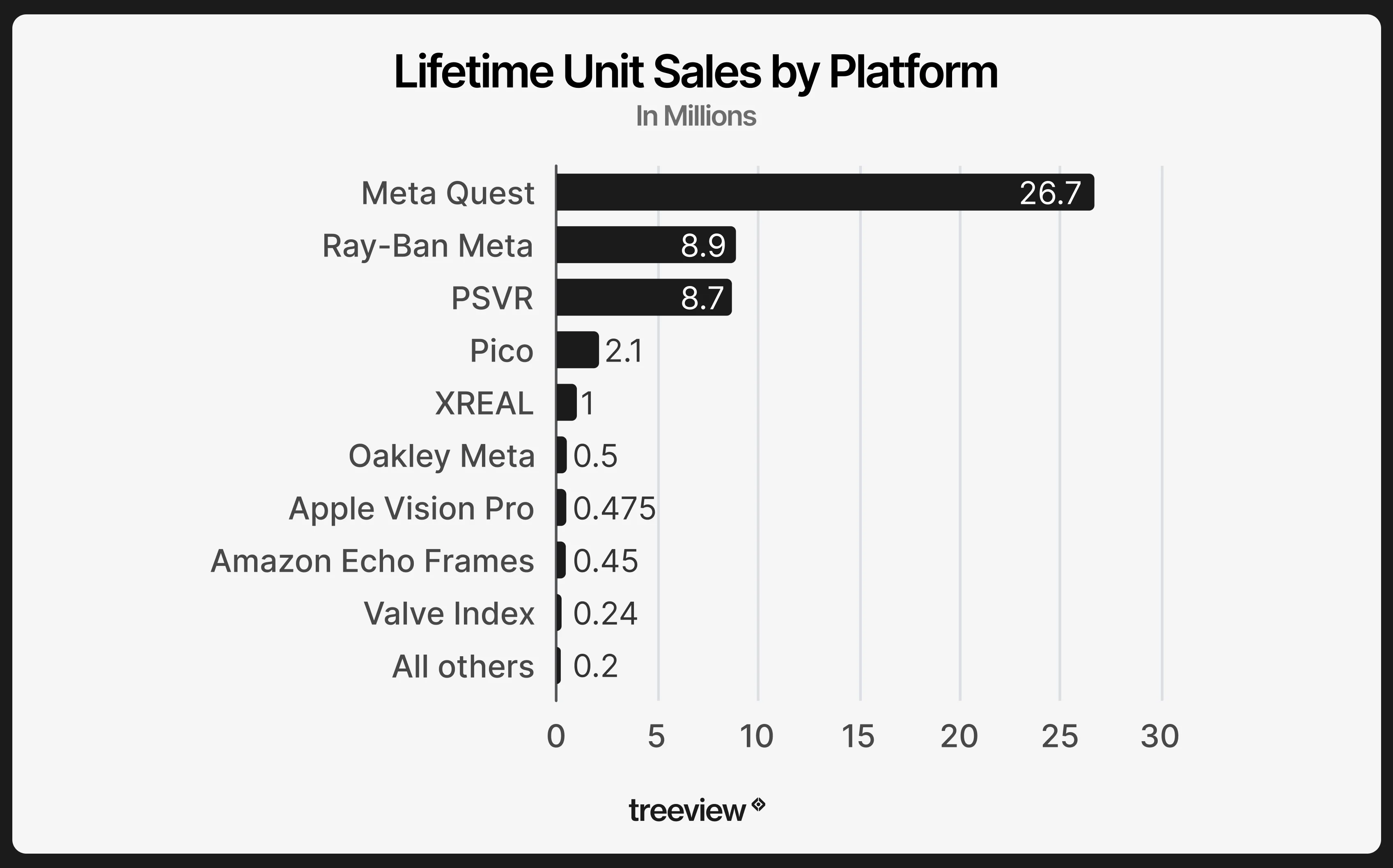

XR Lifetime Units by Platform

Three platforms account for the majority of all XR hardware ever sold: Meta Quest (26.76M), Ray-Ban Meta (8.9M), and PlayStation VR combined (8.7M). Every other platform sits below 2.5M lifetime units. The distance between Meta and the rest of the field is the defining structural fact of XR hardware today.

Platform | Lifetime Units |

|---|---|

Meta Quest (all models) | 26.76M |

Ray-Ban Meta (all generations) | 8.9M |

PSVR1 + PSVR2 combined | 8.7M |

Pico XR | 2.1M |

XREAL | 1.0M |

Oakley Meta | 500K |

Apple Vision Pro | 475K |

Amazon Echo Frames | 450K |

Valve Index | 240K |

RayNeo | 150K |

VITURE | 100K |

Samsung Galaxy XR | 70K |

Brilliant Labs Frame | 22K |

Ray-Ban Meta Display | 20K |

Bigscreen Beyond | 20K |

Snap Spectacles 2024 | 12K |

Varjo XR-4 | 5K |

AjnaLens AjnaXR | 3K |

Total (all 18 platforms) | 49.6M |

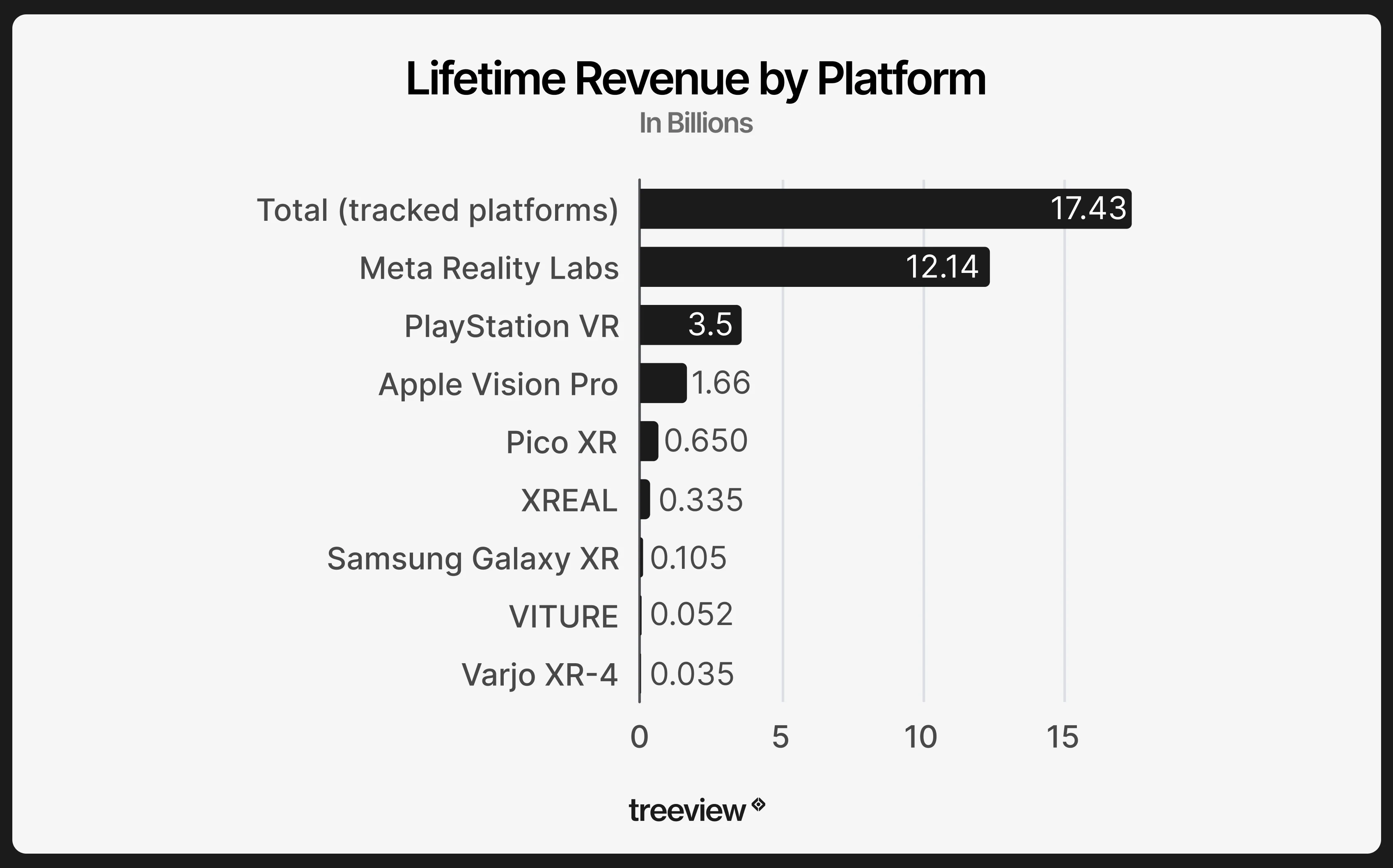

XR Hardware Revenue by Platform

Meta Reality Labs is the only XR hardware division with publicly confirmed annual revenue: $2.27 billion in 2025. All other figures below are derived from unit estimates and average selling prices. The most significant revenue shift of 2025 occurred within Meta itself: smart glasses revenue ($2.15B) exceeded Quest hardware revenue ($660M) for the first time.

Platform | 2025 Revenue (est.) | Lifetime Revenue (est.) |

|---|---|---|

Meta Reality Labs (all) | $2.27B | $12.4B |

↳ Smart glasses (split est.) | $2.15B | $3.5B |

↳ Quest hardware (split est.) | $660M | $7.5B |

PSVR1 + PSVR2 combined | $700M | $3.6B |

Apple Vision Pro | $297M | $1.66B |

XREAL | $145M | $335M |

Pico XR | $90M | $650M |

Samsung Galaxy XR | $60M | $105M |

VITURE | $30M | $52M |

Varjo XR-4 | $20M | $35M |

Total (tracked platforms) | $3.71B | $17.43B |

VR/MR Headsets

Standalone and PC-tethered headsets that fully occlude the real world with a stereoscopic display. This category includes consumer standalone devices, console-tethered headsets, PC VR and enterprise mixed reality systems. Total 2025 shipments: 4.3 million units across all brands.

Platform | Company | Lifetime Units | 2025 Units | YoY | Price |

|---|---|---|---|---|---|

Meta Quest | Meta | 26.76M | 2.3M | -10% est. | $299–$499 |

PSVR1 + PSVR2 | Sony | 8.7M | 1.3M est. | +63% | $549 |

Pico XR | ByteDance | 2.1M | 225K | +13% | — |

Apple Vision Pro | Apple | 475K | 85K | -78% | $3,499 |

Samsung Galaxy XR | Samsung | 70K | 40K | New | $1,799 |

Valve Index | Valve | 240K | 30K | Declining | $999 |

Bigscreen Beyond | Bigscreen | 20K | 10K | — | $1,019 |

Varjo XR-4 | Varjo | 5K | 2K | Flat | $3,990–$9,990 |

Meta

Meta holds 53% of the standalone VR/MR headset market and 75.7% of the combined XR market when smart glasses are included. Its hardware division, Meta Reality Labs, generated $2.27 billion in revenue in 2025 while accumulating roughly $83.6 billion in cumulative operating losses since 2020.

Year | Reality Labs Revenue | Notable Event |

|---|---|---|

2019 | $501M | Quest 1 era |

2020 | $1,139M | Quest 2 launch + pandemic demand |

2021 | $2,274M | Quest 2 peak |

2022 | $2,159M | Quest Pro launched at $1,500, struggled |

2023 | $1,896M | Quest 3 rescued the year at launch |

2024 | $2,146M | Quest 3S, #1 Amazon console in the US |

2025 | $2,270M | Ray-Ban Gen 2 |

Meta Quest

Meta Quest is the dominant VR platform, holding 53% of the standalone headset market. It is the VR ecosystem with the biggest content economy: over 10,000 apps, 300+ titles with $1M+ in lifetime revenue, and more than 1 million Horizon+ subscribers. The Quest 3S at $299 was the top-selling console on Amazon US in Q4 2024.

Metric | Value |

|---|---|

Lifetime units (all models) | 26.76M |

2025 units | 2.3M |

YoY | -10% est. |

MAU (est.) | 8.5M |

Quest Store lifetime revenue | $2.9B |

Beat Saber lifetime revenue | $250M+ |

Gorilla Tag lifetime revenue | $100M+ |

Horizon+ subscribers | 1M+ |

Apps on platform | 10,000+ |

Titles with $1M+ lifetime revenue | 300+ |

The revenue composition inside Reality Labs has fundamentally changed. In 2021, Quest hardware generated roughly $1.85 billion while smart glasses contributed around $45 million. By 2025 those figures had reversed: Quest hardware at $660M, smart glasses at $2.15B.

Model | Launch Price | Lifetime Units | Status |

|---|---|---|---|

Quest 1 | $399 | 1.6M | Discontinued |

Quest 2 | $299 | 20M | Discontinued |

Quest Pro | $1,500 | 100K | Discontinued (failed) |

Quest 3 | $499 | 3.26M (through Q3 2025) | Active |

Quest 3S | $299 | 1.75M (through Q3 2025) | Active |

PlayStation VR

Sony's PlayStation VR franchise is the second-largest VR ecosystem by lifetime units. Its structural advantage is the PlayStation install base: roughly 65 million PS5 owners represent a captive addressable market that no standalone headset manufacturer can match at a comparable price point.

Year | PSVR2 Units | Key Event |

|---|---|---|

2023 | 1.699M | Strong launch |

2024 | 800K | Production pause, PC adapter released |

2025 | 1.3M est. | Recovery: price cuts, new titles, PC mode |

PlayStation VR combines two generations into the second-largest VR ecosystem ever built, with 8.7 million units sold across PSVR1 and PSVR2. After a significant decline in 2024, PSVR2 recovered in 2025 driven by PC adapter support, price reductions and new first-party software. Content revenue reached $280M+ in H1 2025 alone. The platform reports a 40% weekly usage rate and 73% three-month retention, the strongest engagement figures outside Meta Quest.

PSVR1 | PSVR2 | Combined | |

|---|---|---|---|

Launch | Oct 2016 | Feb 2023 | |

Price | $399 | $549 | |

Lifetime units | 5M (final) | 3.7M est. | 8.7M |

Lifetime revenue | $1.75B | $1.83B | $3.58B |

Status | Discontinued | Active |

Pico

Pico is ByteDance's VR headset brand and the dominant player in China's consumer VR market. Its performance is closely tied to ByteDance's appetite for hardware investment, which contracted sharply in 2023–2024 before stabilizing.

Metric | Value |

|---|---|

Lifetime units | 2.1M |

2025 units | 225K |

YoY | +13% |

China market share (H1 2025) | 46% |

Global VR/MR share | 5% |

MAU (est.) | 500K |

Pico held 46% of China's consumer VR market in H1 2025 and 5% of global VR/MR share. The 2023–2024 volume decline reflected both broader VR market weakness and reduced ByteDance investment. The most significant 2026 development: Meta's February 2026 exit from enterprise Quest sales opened a direct lane for Pico's Project Swan in Western enterprise markets, the first credible opportunity Pico has had outside Asia.

Year | Units | Key Event |

|---|---|---|

2021 | 493K | Neo 3 launch |

2022 | 700K | Pico 4 launch |

2023 | 250K | VR market contraction |

2024 | 200K | Pico 4 Ultra launch |

2025 | 225K | Recovery; Meta enterprise exit creates opening |

Total | 2.1M |

Apple Vision Pro

Apple entered XR hardware in February 2024 with Vision Pro, the highest Average Selling Price (ASP) consumer spatial computing device ever shipped. The device is positioned as a productivity and media consumption tool rather than a gaming headset. Enterprise adoption has outpaced consumer adoption since launch.

Metric | Value |

|---|---|

Launch price | $3,499 |

2024 units | 390K |

2025 units | 85K |

Lifetime units | 475K |

Lifetime hardware revenue | $1.66B |

Enterprise buyer share | 75% |

Fortune 100 orgs using AVP | 50+ |

visionOS apps | 3,000+ |

Production status | Halted 2025 |

Apple Vision Pro shipped 390K units in its 2024 launch year, then 85K in 2025 after production was halted at Luxshare early in the year. Despite the volume contraction, Vision Pro has had an outsized influence on the market: it established that buyers will pay premium prices for high-fidelity spatial computing, and it pushed every major competitor to improve passthrough display quality.

Samsung Galaxy XR

Samsung entered the XR headset market in October 2025 with Galaxy XR, running Google's Android XR operating system. The device targets the premium Android ecosystem and is designed as a spatial productivity companion to Galaxy mobile hardware rather than a standalone gaming or enterprise platform.

Metric | Value |

|---|---|

Launch price | $1,799 |

2025 units | 40K |

Lifetime units | 70K |

Lifetime hardware revenue | $105M |

OS | Android XR (Google) |

YoY | New |

2025 revenue | $60M |

Samsung Galaxy XR is the newest major headset platform in this report. At $1,799 and approximately 40K units in 2025, it remains firmly in early-adopter territory. Its strategic significance extends beyond Samsung: Galaxy XR and Android XR represent Google's most serious attempt yet to build a credible spatial computing OS outside of Meta and Apple. If the platform attracts developer investment at scale, it becomes the first viable third option.

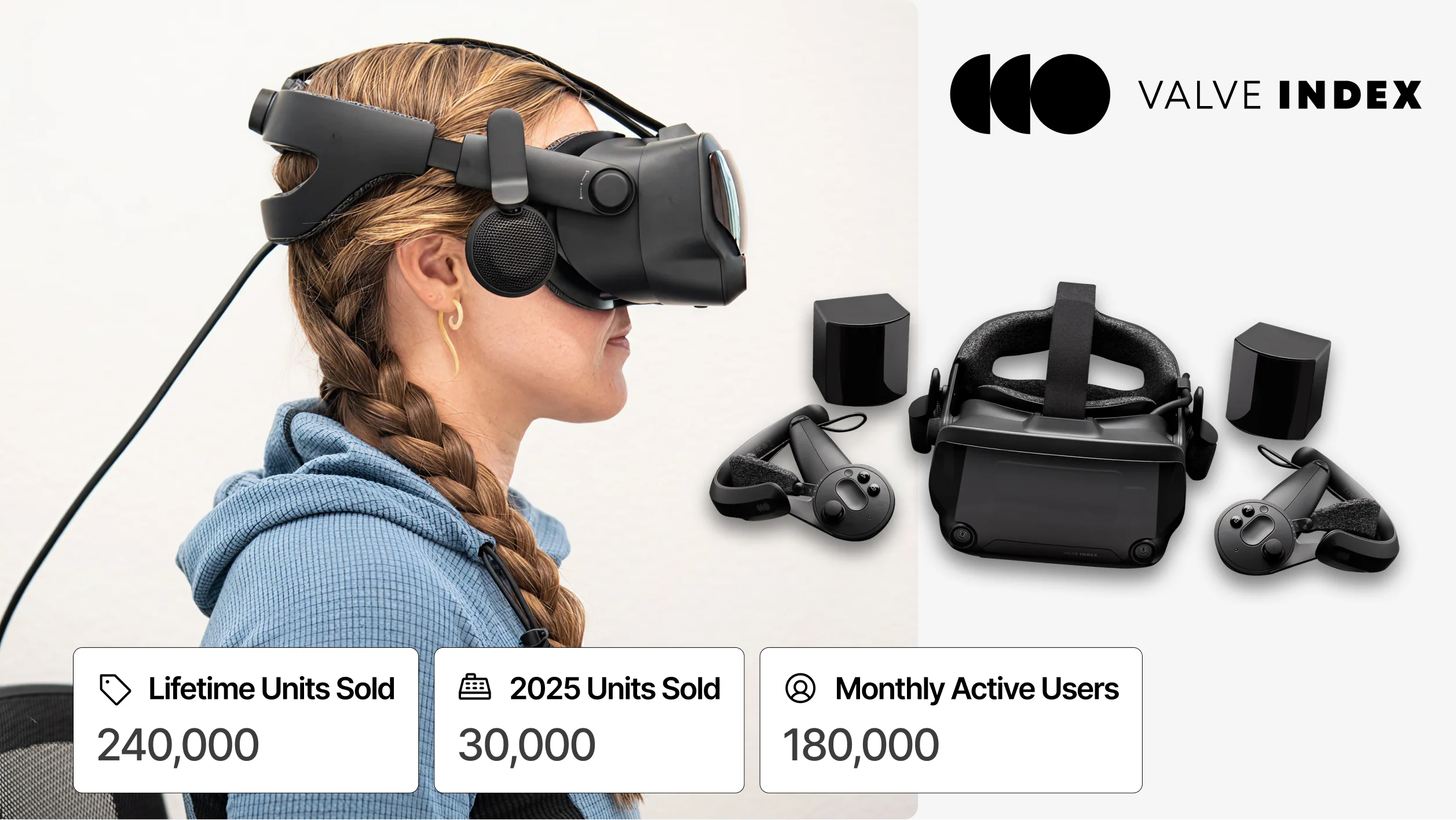

Valve Index

Valve Index is a PC VR headset that requires a gaming PC and SteamVR runtime. It is designed for enthusiast PC gamers who prioritize display fidelity and controller precision. Valve does not publish sales figures; the 240K lifetime estimate is derived from SteamVR hardware survey data.

Metric | Value |

|---|---|

Launch price | $999 (full kit) |

Launch year | 2019 |

Lifetime units | 240K |

2025 units | 30K |

MAU (est.) | 180K |

Trend | Declining |

OS | SteamVR |

Valve confirmed the Index is no longer being manufactured following the announcement of Steam Frame, a standalone headset announced in November 2025 and expected to ship in 2026. Steam Frame represents a fundamental departure from the Index's architecture: where Index required a gaming PC and SteamVR base stations, Frame is a standalone device with inside-out tracking running SteamOS. The 240K lifetime figure for Valve Index should be read as a closing number.

Bigscreen Beyond

Bigscreen makes ultra-compact PC VR headsets for the SteamVR audience that prioritizes weight and form factor over cost. The Beyond 2, at 107g, is the lightest PC VR headset commercially available.

Metric | Value |

|---|---|

Model | Beyond 2 |

Price | $1,019 |

Weight | 107g (lightest PC VR headset) |

Display | Micro-OLED |

2025 units | 10K |

Lifetime units | 20K |

Requires | SteamVR base stations + PC |

Bigscreen Beyond 2 is a micro-OLED PC VR headset designed for users who find conventional headsets too heavy for extended sessions. It requires SteamVR base stations and a capable gaming PC. At $1,019 and 10K units in 2025, it occupies a narrow position within an already small segment, but it represents where PC VR hardware is technically heading: smaller, lighter, higher-resolution.

Varjo XR

Varjo is a Finnish enterprise mixed reality company making headsets at display fidelities that no consumer device approaches. Its hardware is sold directly to enterprise procurement teams in several industries, including defense, automotive, aviation and energy, not through retail channels.

Metric | Value |

|---|---|

Price | $3,990–$9,990 |

Annual subscription | $2,500/device (Base Pro, from Mar 2025) |

Display | 3,840 × 3,744/eye · 51 PPD |

Eye tracking | 200 Hz |

Lifetime units | 5K |

2025 units | 2K |

Key customers | NATO, Airbus, automotive |

Varjo XR-4 is the highest-fidelity commercial MR headset available. The Focal Edition at $9,990 delivers 51 PPD display resolution and 200 Hz eye tracking, specifications that remain far beyond any consumer headset. A significant pricing change took effect in March 2025: a $2,500 per device per year Base Pro subscription became mandatory for chroma key, camera access, 3D reconstruction and passthrough shaders.

AjnaLens AjnaXR

AjnaLens is an Indian XR company whose primary market is government vocational training. Its AjnaXR headset is deployed across 500+ Industrial Training Institutes (ITIs) in India's national skilling network. Nearly all distribution is through government procurement rather than commercial or consumer channels.

Metric | Value |

|---|---|

Price range | $1,020–$1,380 |

Lifetime units | 3K |

Annual subscription | None |

Key customers | 500+ Indian ITIs (govt. vocational training) |

Primary market | India |

Notable 2025 | -58% headcount reduction |

Sales model | Government procurement |

Smart Glasses

AI-enabled, camera-equipped glasses with no optical display. Designed for all-day wear. In 2025, smart glasses shipped 7.25 million units, roughly half the entire XR market. The segment is almost entirely Meta: Ray-Ban Meta and Oakley Meta together account for approximately 97% of AI smart glasses volume.

Platform | Company | Lifetime Units | 2025 Units | YoY | Price |

|---|---|---|---|---|---|

Ray-Ban Meta | Meta | 8.9M | 6.5M | +225% est. | $329 |

Oakley Meta | Meta | 500K | 500K | New | $499–$799 |

Amazon Echo Frames | Amazon | 450K | 150K | Flat | $249–$299 |

Meta

Meta controls the smart glasses market through its hardware partnership with EssilorLuxottica. EssilorLuxottica reported 9 million combined Ray-Ban and Oakley Meta units shipped in full-year 2025. The revenue implications were significant: within Meta's own business, smart glasses revenue ($2.15B) exceeded Quest headset revenue ($660M) for the first time in the company's hardware history.

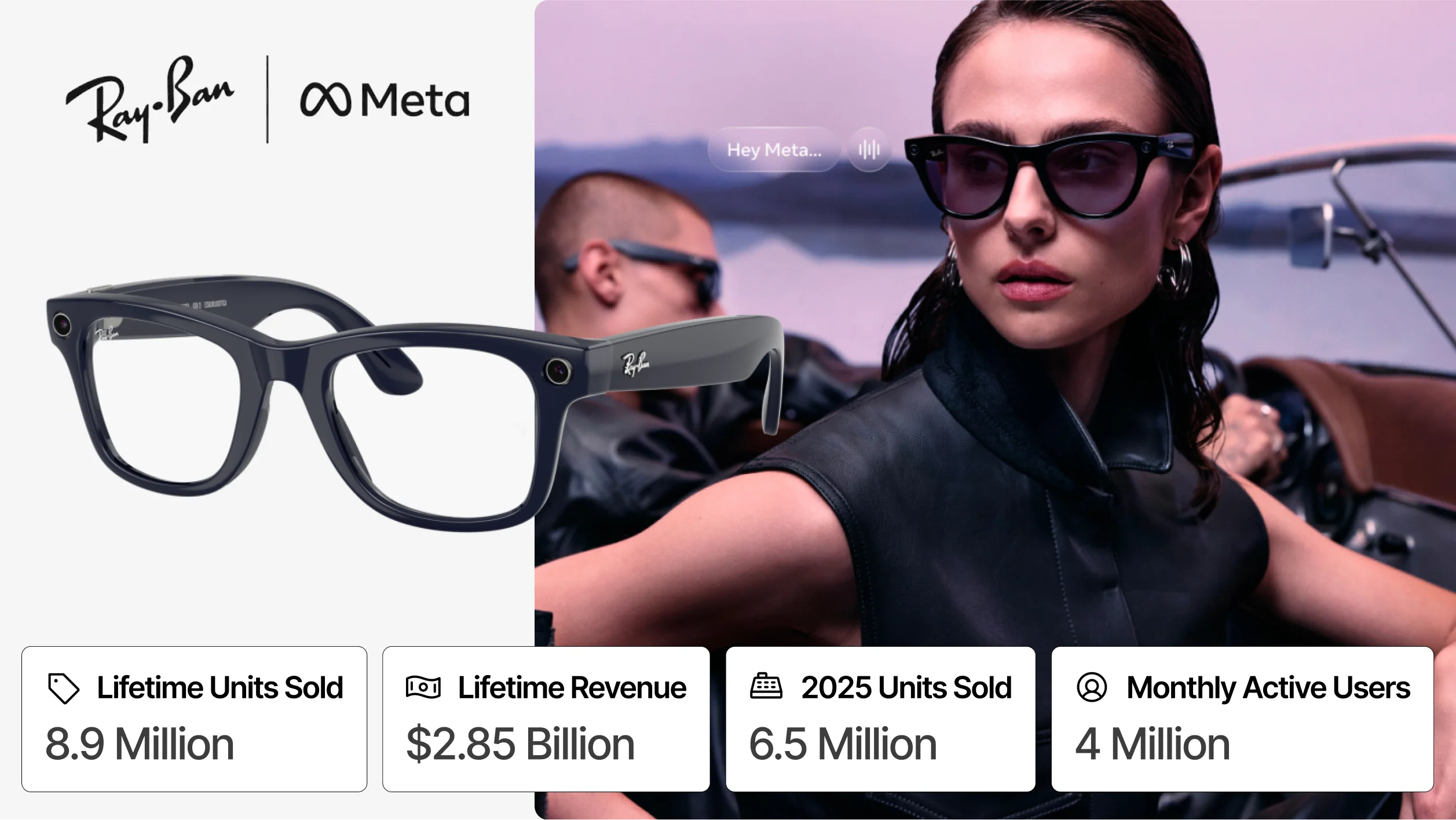

Ray-Ban Meta

Ray-Ban Meta is the best-selling AI smart glasses product in the world. Gen 2 launched in September 2025 with an upgraded camera, Meta AI integration and expanded frame options. It sold an estimated 6.5 million units in its first year, more than the entire AI smart glasses segment shipped in all of 2024.

Metric | Value |

|---|---|

Lifetime units (all generations) | 8.9M |

2025 units | 6.5M |

YoY | +225% est. |

Smart glasses market share (2025) | 90% |

MAU (est.) | 4M |

Lifetime revenue (est.) | $2.85B |

Generation | Launch | Lifetime Units | Price |

|---|---|---|---|

Ray-Ban Stories (Gen 0) | Sep 2021 | 400K | $299 |

Ray-Ban Meta Gen 1 | Oct 2023 | 2M | $299 |

Ray-Ban Meta Gen 2 | Sep 2025 | 6.5M | $329 |

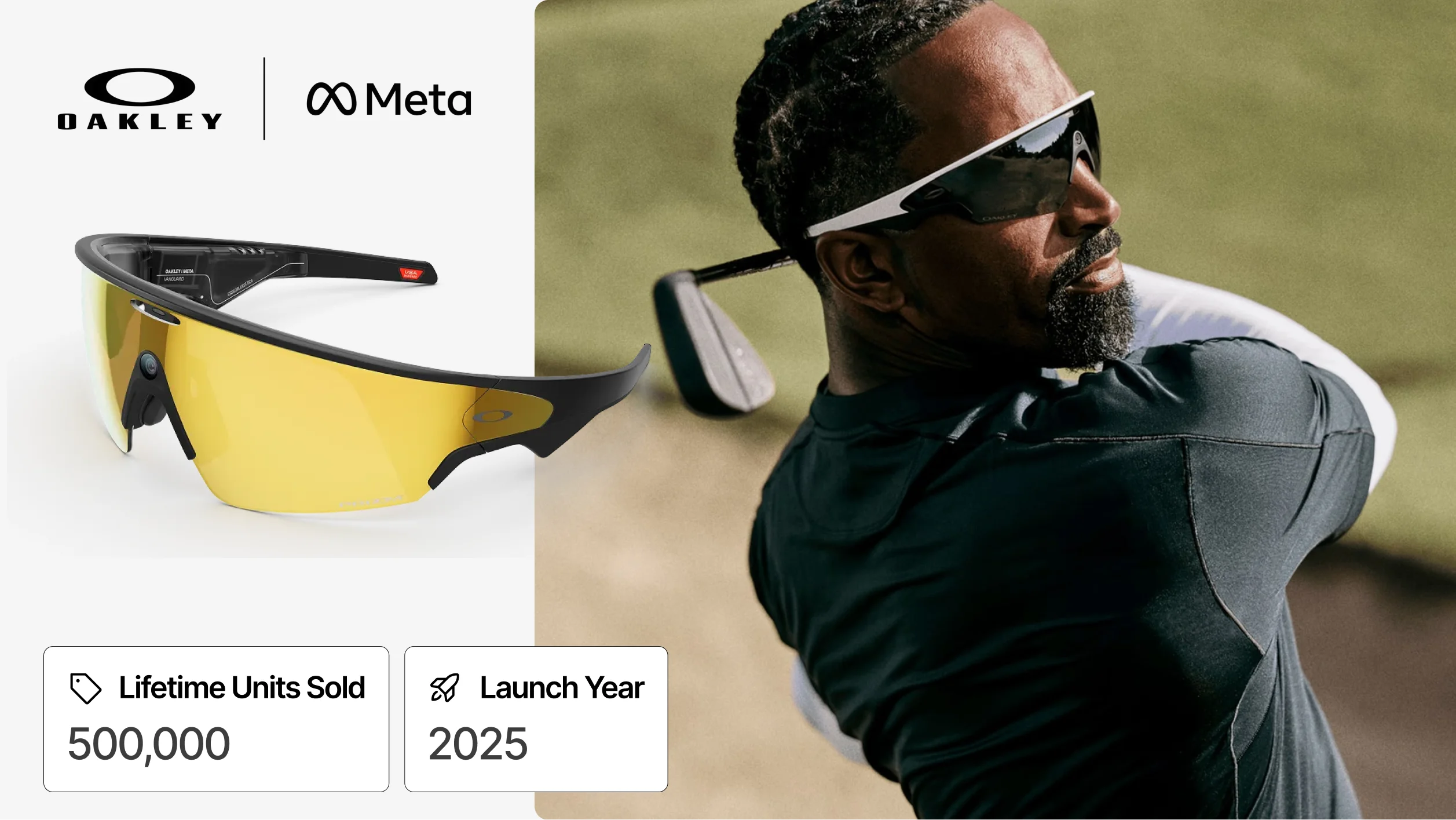

Oakley Meta

Oakley Meta HSTN is the sport and premium tier of Meta's smart glasses lineup, targeting active users for whom the Ray-Ban aesthetic is too lifestyle-oriented. At $499–$799, it carries a higher average selling price than Ray-Ban Meta. It shipped approximately 500K units in its 2025 launch year, immediately becoming the second-largest AI smart glasses product on the market.

Metric | Value |

|---|---|

Model | Oakley Meta HSTN |

Launch year | 2025 |

Price | $499–$799 |

2025 units | 500K |

Lifetime units | 500K |

Smart glasses segment share | 7% |

Status | New |

Amazon Echo Frames

Amazon Echo Frames are audio-only smart glasses with no camera, no AI vision and no display. They predate the current AI smart glasses wave and are excluded from IDC's AI/camera-equipped smart glasses count. The product competes on Alexa integration and all-day wearability rather than on camera or visual AI features.

Metric | Value |

|---|---|

Launch year | 2020 |

Price range | $249–$299 |

Lifetime units | 450K |

2025 units | 150K |

YoY | Flat |

Included in IDC AI glasses count | No (no camera) |

Key feature | Alexa voice assistant |

Echo Frames target Alexa users who want hands-free voice assistant access without carrying a phone. The absence of a camera keeps the form factor low-profile. Growth has been flat as the category's attention has shifted toward Ray-Ban Meta's camera and AI-first positioning.

AR Display Glasses

See-through optical overlay glasses that project digital content into the wearer's field of view while maintaining a direct view of the real world. Display technologies include waveguide and birdbath optics. Total 2025 shipments: approximately 912K units, up roughly 50% from 2024. XREAL has held the #1 market position for four consecutive years.

Platform | Company | Lifetime Units | 2025 Units | Share | Price |

|---|---|---|---|---|---|

XREAL | XREAL | 1.0M | 325K | 36% | $299–$399 |

RayNeo | TCL | 150K | 75K | 8% | — |

VITURE | VITURE | 100K | 55K | 6% | — |

Ray-Ban Meta Display | Meta | 20K | 20K | 2% | $799 |

Brilliant Labs Frame | Brilliant Labs | 22K | 11K | 1% | $349 |

Snap Spectacles 2024 | Snap | 12K | 12K | 1% | $99/mo |

AjnaLens AjnaXR | AjnaLens | 3K | 2K | <1% | $1,020–$1,380 |

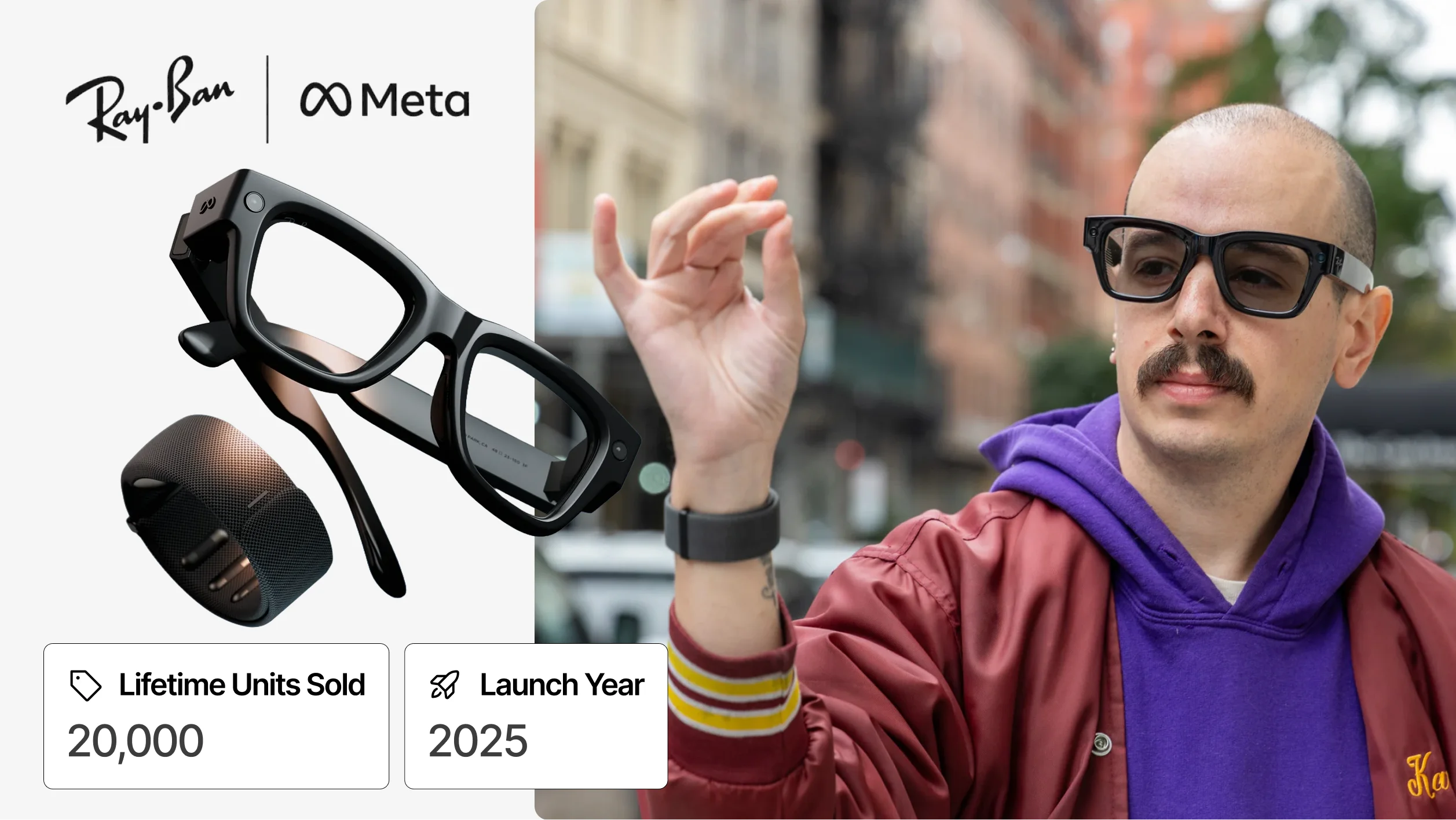

Meta Ray-Ban Display

Meta's entry into AR display glasses is the Meta Ray-Ban Display, a waveguide AR product at $799 positioned above the standard Ray-Ban Meta smart glasses line. Unlike the standard Ray-Ban Meta, which carries no display, the Display version projects a visible screen overlay. Its 20K units are counted in the AR display segment, separate from the 7.25M smart glasses figure.

Metric | Value |

|---|---|

Launch year | 2025 |

Price | $799 |

Display technology | Waveguide AR overlay |

2025 units | 20K |

Lifetime units | 20K |

AR display segment share | 2% |

Counted in smart glasses 7.25M? | No |

Meta Ray-Ban Display tests consumer appetite for a display-equipped version of the Ray-Ban form factor. At $799 and roughly 20K units in its 2025 launch, it remains a limited release rather than a volume product. Its significance is strategic: it signals that Meta is exploring both ends of the glasses spectrum, camera-only at scale and AR display at premium.

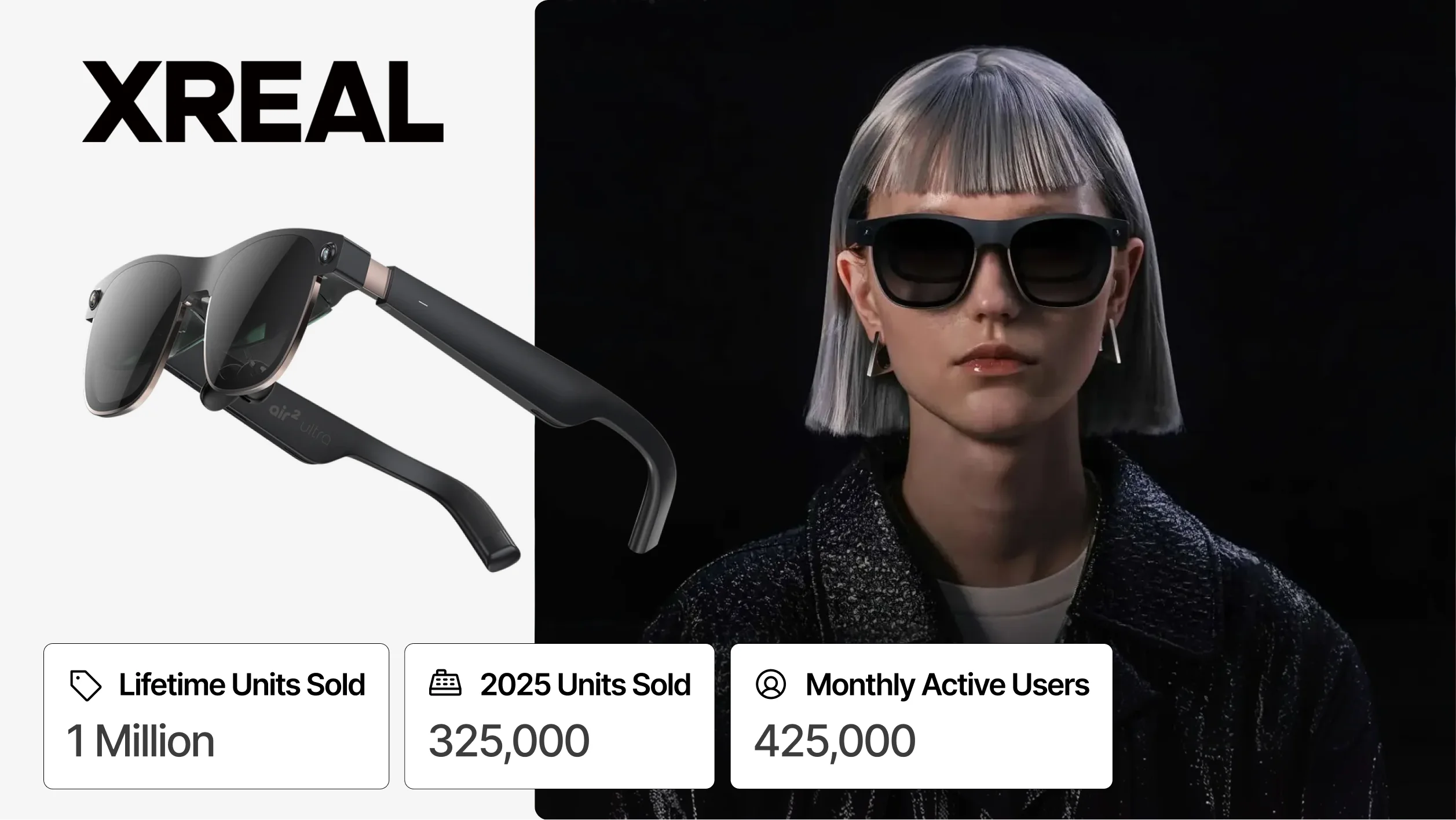

XREAL

XREAL is the dominant AR display glasses brand globally, holding the top market share position for four consecutive years. Its distribution reaches consumers through direct online sales and partnerships with telecom carriers and gaming platforms across multiple regions.

Metric | Value |

|---|---|

Lifetime units | 1.0M |

2025 units | 325K |

YoY | +63% |

Global AR display share | 36% |

North America AR share (Q2 2025) | 43.9% |

MAU (est.) | 425K |

Consecutive years at #1 | 4 |

XREAL confirmed 700K+ lifetime units in June 2025 and likely crossed 1 million by year end. It holds 36% of the global AR display glasses market and 43.9% of the North America segment as of Q2 2025. The XREAL One series, priced at $299–$399, has been the primary volume driver, a price point low enough to reach enthusiast consumers without requiring enterprise sales cycles.

Year | Units | Revenue (est.) |

|---|---|---|

2022 | 100K | $38M |

2023 | 200K | $72M |

2024 | 200K | $80M |

2025 | 325K | $145M |

RayNeo

RayNeo is a TCL subsidiary and the third-largest AR display glasses brand by 2025 shipments. Its X3 Pro targets enterprise and prosumer users with waveguide optics and holds approximately 8% of the global AR display segment.

Metric | Value |

|---|---|

Parent company | TCL |

Key product | RayNeo X3 Pro |

2025 units | 75K |

Lifetime units | 150K |

AR display segment share | 8% |

Primary markets | China, enterprise |

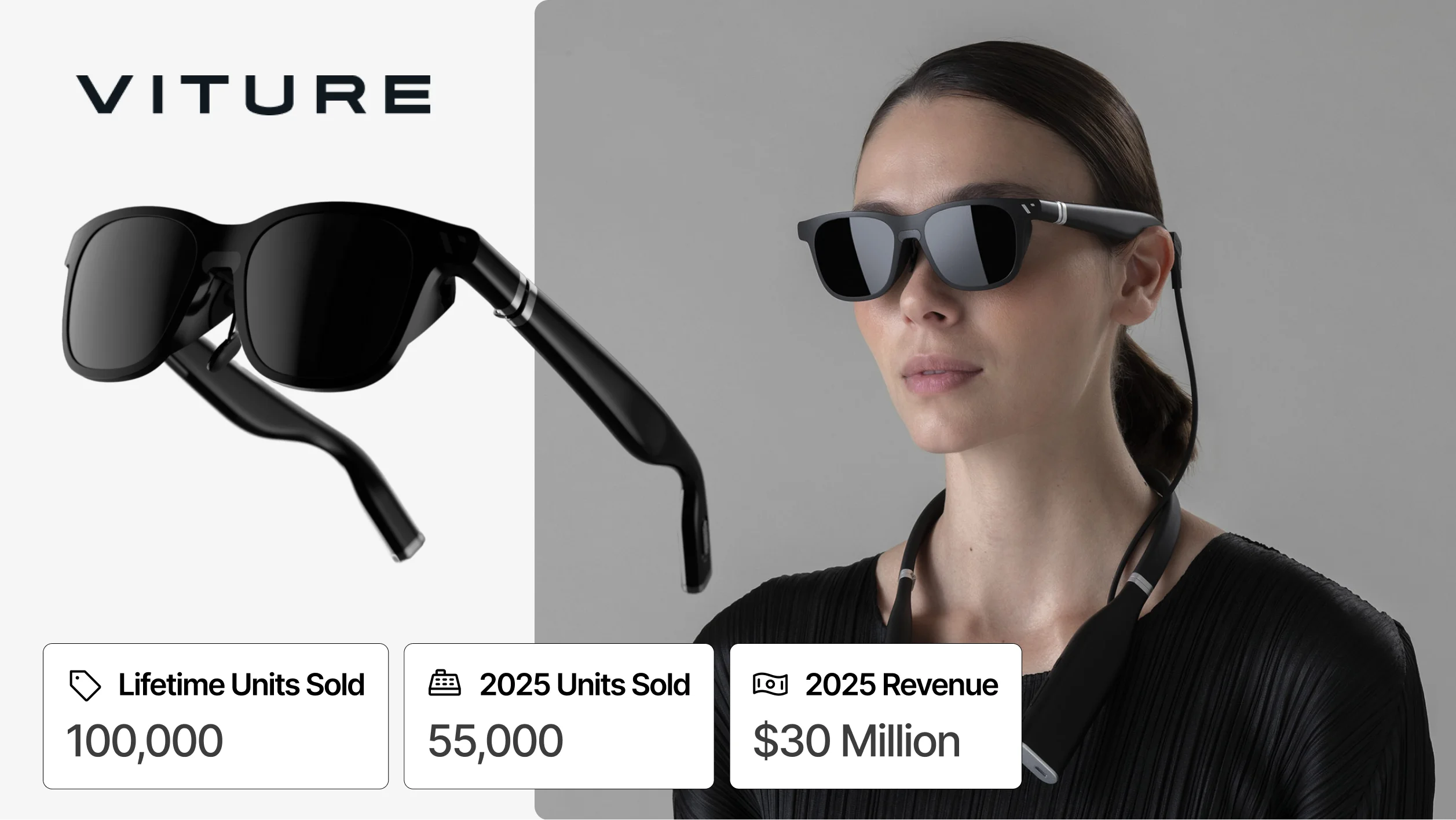

VITURE

VITURE positions its AR display glasses as a portable big-screen replacement for gaming and media consumption rather than an enterprise or productivity tool. Its birdbath optics deliver a wider field of view than waveguide alternatives at lower manufacturing cost.

Metric | Value |

|---|---|

Key product | VITURE One |

Optics | Birdbath |

2025 units | 55K |

Lifetime units | 100K |

AR display segment share | 6% |

2025 revenue (est.) | $30M |

Primary use case | Gaming / media |

Brilliant Labs Frame

Brilliant Labs makes open-source AR glasses built around developer access and AI integration. Frame is the most open AR hardware platform commercially available, with a Python SDK and a community-built AI assistant called Noa.

Metric | Value |

|---|---|

Price | $349 |

SDK | Python (open-source) |

AI assistant | Noa (built-in) |

2025 units | 11K |

Lifetime units | 22K |

AR display segment share | 1% |

Hardware | Open-source |

Frame is a lightweight, open-source AR glasses product at $349. The full hardware and software stack is open-source, and the built-in Noa AI assistant is community-developed. At approximately 11K units in 2025, it functions as a developer and researcher platform rather than a consumer product, but it represents the open-source end of the AR glasses market and influences how the broader developer community thinks about wearable AI hardware.

Snap Spectacles 2024

Snap's Spectacles 2024 are an AR display glasses product distributed through a developer subscription program rather than retail channels. With waveguide optics and a built-in AI assistant, they project digital overlays into the wearer's field of view, making them AR display glasses by technical definition. Snap is using the developer program to seed the platform ahead of an anticipated consumer launch.

Metric | Value |

|---|---|

Display technology | Waveguide AR overlay |

Access model | $99/month subscription (dev program) |

2025 units | 12K |

Lifetime units | 12K |

AR display segment share | 1% |

Status | Dev program only |

Consumer version | Expected 2026 |

Spectacles 2024 are available through a $99/month developer subscription, limiting distribution to creators and builders. The approximately 12K units shipped in 2025 represent platform seeding rather than commercial scale. A consumer version is expected in 2026, at which point Spectacles will move from this emerging tier into the mainstream AR display segment.

Where the XR Market Stands in 2026

Smart glasses won the volume race not because they are the most technically capable XR device, but because they are the most wearable one. They outsold VR/MR headsets by a ratio of roughly 3:1 in 2025. That gap is likely to widen before it narrows.

Meta's dominance is deeper than it looks. Meta holds 75.7% of XR shipment volume, but its strategic position is more concentrated than even that number suggests. Ray-Ban Meta smart glasses generated an estimated $2.15B in hardware revenue in 2025, more than Quest for the first time ever. Meta now has two separate high-volume product lines in two separate XR categories. No other company has one, but that is about to change.

Two significant launches in the smart glasses market are taking shape simultaneously. The first is Apple. Reports as of early 2026 suggest there are no Apple Vision headsets in active development, with the company's focus pivoting decisively toward smart glasses. Bloomberg reported that Apple is aiming to release smart glasses by end of 2026 as part of a broader push into AI-enhanced products. The first model will match Ray-Ban Meta's camera, microphone and AI feature set, with Siri serving as the primary interface.

The second launch is Android XR. Samsung confirmed at MWC that it is targeting an AI-powered smart glasses launch in 2026, built in partnership with Google and Qualcomm, featuring a camera and microphone and tethered to a smartphone. Samsung is reportedly developing two distinct models, both expected to ship in 2026, potentially weighing as little as 50 grams, with deep integration with Google's Gemini AI assistant. Google's retail versions are being co-developed with Warby Parker and Gentle Monster, and a monocular display version is also planned for 2026.

The picture that emerges is not one where Meta loses, but one where the smart glasses category becomes genuinely competitive for the first time. In 2025, Meta owned it almost entirely. By end of 2026, there will likely be at least three major ecosystems: Meta/Ray-Ban, Android XR/Samsung and Apple, all competing for the same wrist, the same face and the same daily-wear use cases. That transition is the most consequential development in XR hardware in years.

Frequently Asked Questions (FAQs) about the XR and Smart Glasses Market

Q1. What is the size of the XR market in 2026?

The global extended reality (XR) market reached an estimated $20.43 billion in 2025. This includes hardware such as VR headsets, AR glasses and AI smart glasses, along with platform ecosystems and software revenue. Market forecasts project XR to grow to more than $85 billion by 2030 as spatial computing devices become more mainstream.

Q2. How many XR devices were sold in 2025?

Approximately 14.5 million XR devices were shipped globally in 2025, representing a 41.6% year-over-year increase. Most of this growth came from AI-powered smart glasses rather than traditional VR headsets.

Q3. What are the most popular XR headsets and smart glasses?

The largest XR platforms by lifetime device sales include:

Meta Quest – 26.76 million units

Ray-Ban Meta smart glasses – 8.9 million units

PlayStation VR – 8.7 million units

Pico VR headsets – 2.1 million units

XREAL AR glasses – 1 million units

Meta currently dominates the XR hardware ecosystem.

Q4. Are smart glasses replacing VR headsets?

Smart glasses are currently growing faster than VR headsets because they are lighter, more wearable, and designed for everyday use. In 2025, smart glasses accounted for about 50% of all XR device shipments, while VR and mixed reality headsets represented roughly 30% of the market.

Q5. How many people use XR technology?

Industry projections estimate that 3.7 billion people could be using XR technologies by 2029, including AR glasses, VR headsets, spatial computing devices and AI wearables.

Q6. Which company leads the XR hardware market?

Meta is the dominant company in the XR hardware market, controlling approximately 75% of total XR device shipments when both VR headsets and smart glasses are included. Its two major platforms are: Meta Quest VR headsets and Ray-Ban Meta AI smart glasses.

Q7. What is spatial computing?

Spatial computing refers to technologies that blend digital content with the physical world, enabling interaction through devices like VR headsets, AR glasses and mixed reality headsets. These systems use sensors, cameras and AI to understand the user’s environment and display interactive digital information.

Q8. What is the difference between VR, AR, MR and smart glasses?

The XR ecosystem includes several types of devices:

Virtual Reality (VR) – fully immersive headsets that block the real world.

Augmented Reality (AR) – glasses that overlay digital information onto the real world.

Mixed Reality (MR) – headsets that blend digital objects with the physical world, allowing virtual elements to interact with real environments in real time.

Smart Glasses – wearable AI devices with cameras and voice assistants but no display.

Each category serves different use cases such as gaming, productivity, navigation, or communication.

Q9. What is the most popular VR headset platform?

The Meta Quest platform is currently the largest VR ecosystem. It has: more than 26 million lifetime headset sales, over 10,000 native VR apps and hundreds of titles generating over $1 million in revenue. It remains the dominant standalone VR platform globally.

Q10. How successful is Apple Vision Pro?

Apple Vision Pro launched in 2024 with a $3,499 price point, positioning it as a premium spatial computing device. By the end of 2025, it had sold roughly 475,000 units, generating about $1.66 billion in hardware revenue and establishing Apple as a major player in the XR ecosystem.

Q11. Which AR glasses companies lead the market?

The AR display glasses market is led by:

XREAL, which holds roughly 36% of the global AR display glasses market

RayNeo (TCL)

VITURE

These devices project digital overlays into the user’s field of view while maintaining visibility of the real world.

Q12. What industries are adopting XR technology?

XR technology is increasingly used across multiple industries, including:

manufacturing and industrial training,

healthcare and medical simulation,

retail and immersive commerce,

architecture and construction,

entertainment and gaming.

Many Fortune 500 companies already use XR for training, visualization and product design.

Q13. Why are smart glasses growing so quickly?

Smart glasses are expanding rapidly because they are lightweight, socially acceptable and designed for everyday use. Unlike VR headsets, they can be worn throughout the day and integrate features such as cameras, voice assistants and AI-powered search.

Q14. What major XR devices are expected to launch next?

Several major XR product launches are expected in the near future, including:

Apple smart glasses expected around 2026

Android XR smart glasses from Samsung and Google

New spatial computing platforms built around AI assistants.

Q15. What is the future of the XR market?

The XR market is expected to evolve from niche headsets into mainstream wearable computing platforms. Smart glasses, spatial computing devices and AI-powered wearables will likely drive the next wave of adoption as companies compete to build the dominant ecosystem.

Q16. Who are the top companies developing solutions for the XR industry?

The XR ecosystem includes both hardware manufacturers and top XR software development studios building virtual reality, augmented reality, mixed reality and spatial computing solutions.

Some of the most influential companies in the industry include:

Meta – developer of the Meta Quest VR platform and Ray-Ban Meta smart glasses.

Apple – creator of the Vision Pro spatial computing headset and the visionOS ecosystem.

Sony – maker of the PlayStation VR headset platform.

Samsung – developing Android XR headsets and smart glasses in partnership with Google.

ByteDance (Pico) – manufacturer of Pico VR headsets and XR ecosystem in Asia.

XREAL – global leader in AR display glasses for consumers and developers.

Varjo – developer of high-fidelity enterprise mixed reality headsets used in industries like aviation and defense.

Snap – building AR glasses platforms through its Spectacles developer ecosystem.

In addition to hardware manufacturers, XR development studios build spatial computing applications for enterprise and consumer use cases. Companies such as Treeview, an XR studio focused on building spatial computing software for Fortune 500 enterprises, develop immersive applications using technologies like Unity and Digital Twins across industries including healthcare, retail, manufacturing and training.

Sources and Methodology

Unit sales figures for Meta Quest and Ray-Ban Meta are drawn directly from Meta's quarterly earnings calls and EssilorLuxottica investor disclosures, the only XR platforms with audited public financials and confirmed shipment numbers. PSVR2 figures combine Sony's official milestone announcements with IDC channel shipment data. Because the two methodologies measure different things (sell-through to consumers vs. shipments into retail), both figures are preserved in the report with the discrepancy explained inline.

Apple Vision Pro production and sales data comes from IDC, supply chain reporting by Bloomberg and The Information, and Luxshare assembly disclosures. All other platform figures, including Pico XR, XREAL, RayNeo, VITURE, Varjo and Samsung Galaxy XR, are sourced from IDC and Counterpoint Research analyst reports, cross-referenced against company press releases and trade coverage from UploadVR, Road to VR and The Verge where available.

Revenue figures for every platform except Meta Reality Labs are estimates derived from unit counts multiplied by average selling price. They should be treated as approximations, not audited financials. MAU figures are estimates based on platform engagement disclosures, SteamVR hardware survey data and third-party app analytics. Platforms that publish no engagement data are labeled as estimates throughout.

Market share percentages reference IDC Q3 2025 unless a source specifies a different period. All lifetime unit figures reflect hardware sold through Q4 2025.

IDC — Worldwide Quarterly Augmented and Virtual Reality Headset Tracker Q3 2025, Dec 2025

IDC — Worldwide Quarterly Augmented and Virtual Reality Headset Tracker Q2 2025, Sep 2025

IDC — Worldwide Quarterly Augmented and Virtual Reality Headset Tracker Q1 2025, Jun 2025

IDC — Q3 2025 XR Tracker: Meta 75.7% Share, XREAL 2% in Display Glasses

TelecomLead — Global AR/VR and Smart Glasses Shipments to Surge 39% in 2025, IDC, Sep 2025

Road to VR — Meta Quest Store Passes $2.9B in All-Time Revenue, Apr 2025

Road to VR — PSVR2 Six-Week Sales Beat Original PSVR, May 2023

Road to VR — Meta Ends Commercial Quest Sales, Shuts Down Workrooms, Jan 2026

IconEra — PlayStation Statistics including PSVR2 Sales Data, 2025

China Daily (gov) — XREAL Surpasses 700K Lifetime Units, Sep 2025

MacRumors — Apple Vision Pro IDC Sales Data 2024–2025, Jan 2026

UploadVR — Meta Explicitly Separating Horizon Worlds From Quest, Feb 2026

UploadVR — Meta Has Sold Nearly 20 Million Quest Headsets (Leak), Mar 2023

Game Developer — Meta Has Sold Almost 20 Million Quest Headsets, Feb 2023

Mordor Intelligence — Extended Reality Market Forecast 2025–2031, 2025

Meta for Work — Accenture VR Onboarding: One Accenture Park Case Study